Lenovo 2011 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2011 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

2010/11 Annual Report Lenovo Group Limited

90

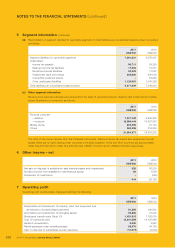

NOTES TO THE FINANCIAL STATEMENTS (continued)

2 Significant accounting policies (continued)

(t) Revenue (continued)

(ii) Interest income

Interest income is recognized using the effective interest method. When a receivable is impaired, the Group

reduces the carrying amount to its recoverable amount, being the estimated future cash flow discounted at the

original effective interest rate of the instrument, and continues unwinding the discount as interest income. Interest

income on impaired receivables is recognized using the original effective interest rate.

(iii) Dividend income

Dividend income is recognized when the right to receive payment is established.

(u) Non-base manufacturing costs

Non-base manufacturing costs are costs that are periodic in nature as opposed to product specific. They are typically

incurred after the physical completion of the product and include items such as outbound freight for in-country finished

goods shipments, warranty costs, engineering changes, storage and warehousing cost, and contribute to bringing

inventories to their present location and condition. Non-base manufacturing costs enter into the calculation of gross

margin but are not inventoriable costs.

(v) Employee benefits

(i) Pension obligations

The Group operates various pension schemes. The schemes are generally funded through payments to insurance

companies or trustee-administered funds, determined by periodic actuarial calculations. The Group has both

defined benefit and defined contribution plans. A defined contribution plan is a pension plan under which the

Group pays fixed contributions into a separate entity. The Group has no legal or constructive obligations to

pay further contributions if the fund does not hold sufficient assets to pay all employees the benefits relating to

employee service in the current and prior periods. A defined benefit plan is a pension plan that is not a defined

contribution plan. Typically, defined benefit plans define an amount of pension benefit that an employee will receive

on retirement, usually dependent on one or more factors such as age, years of service and compensation.

The liability recognized in the balance sheet in respect of defined benefit pension plans is the present value of the

defined benefit obligation at the balance sheet date less the fair value of plan assets, together with adjustments

for unrecognized past service costs. Significant portion of the defined benefit obligation is calculated annually by

independent actuaries using the projected unit credit method. The present value of the defined benefit obligation

is determined by discounting the estimated future cash outflows using interest rates of high-quality corporate or

government bonds that are denominated in the currency in which the benefits will be paid, and that have terms to

maturity approximating to the terms of the related pension liability. In countries where there is no deep market in

such bonds, the market rates on government bonds are used.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are charged

or credited to other comprehensive income in the year they arise.

Past service costs are recognized immediately in income, unless the changes to the pension plan are conditional

on the employees remaining in service for a specified period of time (the vesting period). In this case, the past

service costs are amortized on a straight-line basis over the vesting period.

For defined contribution plans, the Group pays contributions to publicly or privately administered pension insurance

plans on a mandatory, contractual or voluntary basis. The Group has no further payment obligations once the

contributions have been paid. The contributions are recognized as employee benefit expense when they are due

and are reduced by employer’s portion of voluntary contributions forfeited by those employees who leave the

scheme prior to vesting fully. Prepaid contributions are recognized as an asset to the extent that a cash refund or

a reduction in the future payments is available.

The Group’s contributions to local municipal government retirement schemes in connection with retirement benefit

schemes in the Mainland of China (“Chinese Mainland”) are expensed as incurred. The local municipal governments

in the Chinese Mainland assume the retirement benefit obligations of the qualified employees.