Kodak 2012 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2012 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

|

|

Table of Contents

Properties are recorded at cost, net of accumulated depreciation. Kodak capitalizes additions and improvements. Maintenance and repairs are

charged to expense as incurred. Kodak calculates depreciation expense using the straight-line method over the assets’ estimated useful lives,

which are as follows:

Kodak depreciates leasehold improvements over the shorter of the lease term or the asset’s estimated useful life. Upon sale or other disposition,

the applicable amounts of asset cost and accumulated depreciation are removed from the accounts and the net amount, less proceeds from

disposal, is charged or credited to net (loss) earnings.

GOODWILL

Goodwill represents the excess of purchase price of an acquisition over the fair value of net assets acquired. Goodwill is not amortized, but is

required to be assessed for impairment at least annually. Kodak has elected September 30 as the annual impairment assessment date for all of its

goodwill reporting units, and will perform additional impairment tests when events or changes in circumstances occur that would more likely

than not reduce the fair value of the reporting unit below its carrying amount. A reporting unit is defined as an operating segment or one level

below an operating segment. Kodak estimates the fair value of its reporting units using income and market approaches, through the application

of discounted cash flow and market comparable methods, respectively. The assessment is required to be performed in two steps, step one to test

for a potential impairment of goodwill and, if potential losses are identified, step two to measure the impairment loss. Determining the fair value

of a reporting unit involves the use of significant estimates and assumptions. Refer to Note 8, “Goodwill and Other Intangible Assets.”

REVENUE

Kodak’s revenue transactions include sales of the following: products; equipment; software; services; integrated solutions; and intellectual

property licensing. Kodak recognizes revenue when realized or realizable and earned, which is when the following criteria are met:

(1) persuasive evidence of an arrangement exists; (2) delivery has occurred; (3) the sales price is fixed or determinable; and (4) collectability is

reasonably assured. If Kodak determines that collection of a fee is not reasonably assured, the fee is deferred and revenue is recognized at the

time collection becomes reasonably assured, which is generally upon receipt of payment. At the time revenue is recognized, Kodak provides for

the estimated costs of customer incentive programs, warranties and estimated returns and reduces revenue accordingly. Kodak accrues the

estimated cost of post-sale obligations, including basic product warranties, based on historical experience at the time Kodak recognizes revenue.

For product sales, the revenue recognition criteria are generally met when title and risk of loss have transferred from Kodak to the buyer, which

may be upon shipment or upon delivery to the customer site, based on contract terms or legal requirements in certain jurisdictions.

For equipment sales, the recognition criteria are generally met when the equipment is delivered and installed at the customer site. Revenue is

recognized for equipment upon delivery as opposed to upon installation when the equipment has stand-alone value to the customer, and the

amount of revenue allocable to the equipment is not legally contingent upon the completion of the installation. In instances in which the

agreement with the customer contains a customer acceptance clause, revenue is deferred until customer acceptance is obtained, provided the

customer acceptance clause is considered to be substantive. For certain agreements, Kodak does not consider these customer acceptance clauses

to be substantive because Kodak can and does replicate the customer acceptance test environment and performs the agreed upon product testing

prior to shipment. In these instances, revenue is recognized upon installation of the equipment.

Revenue from the sale of software licenses is recognized when; (1) Kodak enters into a legally binding arrangement with a customer for the

license of software; (2) Kodak delivers the software; (3) customer payment is deemed fixed or determinable and free of contingencies or

significant uncertainties; and (4) collection from the customer is probable. Software maintenance and support revenue is recognized ratably over

the term of the related maintenance contract.

Revenue from services includes extended warranty, customer support and maintenance agreements, consulting, business process services,

training and education. Service revenue is recognized over the contractual period or as services are performed. In

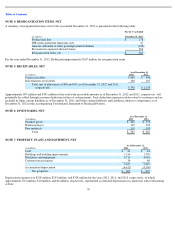

65

Years

Buildings and building improvements

5

-

40

Land improvements

20

Leasehold improvements

3

-

20

Equipment

3

-

15

Tooling

1

-

3

Furniture and fixtures

5

-

10