Kodak 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

|

|

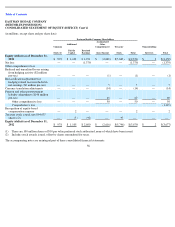

Table of Contents

its business. Successful implementation of Kodak’s plan, however, is subject to numerous risks and uncertainties. In addition, the increasingly

competitive industry conditions under which Kodak operates have negatively impacted Kodak’s results of operations and cash flows and may

continue to do so in the future. These factors raise substantial doubt about Kodak’s ability to continue as a going concern.

The accompanying consolidated financial statements have been prepared assuming that Kodak will continue as a going concern and contemplate

the realization of assets and the satisfaction of liabilities in the normal course of business. Kodak’s ability to continue as a going concern is

contingent upon Kodak’s ability to comply with the financial and other covenants contained in the DIP Credit Agreement, the Bankruptcy

Court’s approval of the Company’s reorganization plan and the Company’s ability to successfully implement the Company’s plan and obtain

exit financing, and maintain sufficient liquidity, among other factors. As a result of the Bankruptcy Filing, the realization of assets and the

satisfaction of liabilities are subject to uncertainty. While operating as debtors-in-possession under chapter 11, the Company may sell or

otherwise dispose of or liquidate assets or settle liabilities, subject to the approval of the Bankruptcy Court or as otherwise permitted in the

ordinary course of business (and subject to restrictions contained in the DIP Credit Agreement), for amounts other than those reflected in the

accompanying consolidated financial statements. Further, the reorganization plan could materially change the amounts and classifications of

assets and liabilities reported in the consolidated financial statements. The accompanying consolidated financial statements do not include any

adjustments related to the recoverability and classification of assets or the amounts and classification of liabilities or any other adjustments that

might be necessary should Kodak be unable to continue as a going concern or as a consequence of the Bankruptcy Filing.

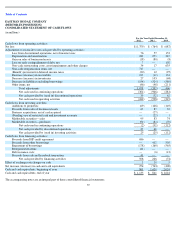

NOTE 2: SIGNIFICANT ACCOUNTING POLICIES

ACCOUNTING PRINCIPLES

The consolidated financial statements and accompanying notes are prepared in accordance with accounting principles generally accepted in the

United States of America. The following is a description of the significant accounting policies of Kodak.

BASIS OF CONSOLIDATION

The consolidated financial statements include the accounts of Eastman Kodak Company (“EKC” or the “Company”), its wholly owned

subsidiaries, and its majority owned subsidiaries (collectively “Kodak”). Kodak consolidates variable interest entities if Kodak has a controlling

financial interest and is determined to be the primary beneficiary of the entity. Kodak accounts for investments in companies over which it has

the ability to exercise significant influence, but does not hold a controlling interest, under the equity method of accounting, and Kodak records

its proportionate share of income or losses in Other income (charges), net in the accompanying Consolidated Statements of Operations. Kodak

accounts for investments in companies over which it does not have the ability to exercise significant influence under the cost method of

accounting. These investments are carried at cost and are adjusted only for other-than-temporary declines in fair value. Kodak has eliminated all

significant intercompany accounts and transactions, and net earnings are reduced by the portion of the net earnings of subsidiaries applicable to

non-controlling interests.

Certain amounts for prior periods have been reclassified to conform to the current period classification due to changes in Kodak’s segment

reporting structure and the presentation of discontinued operations. Refer to Note 26, “Segment Information” and Note 25, “Discontinued

Operations” for additional information.

USE OF ESTIMATES

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires

management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and

liabilities at year end, and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those

estimates.

CHANGE IN ESTIMATE

In conjunction with Kodak’s goodwill impairment analysis in the fourth quarter of 2010, Kodak reviewed its estimates of the remaining useful

lives of its then Film, Photofinishing and Entertainment Group segment’s long-lived assets. This analysis indicated that overall these assets will

continue to be used in these businesses for a longer period than anticipated in 2008, the last time that depreciable lives were adjusted for these

assets. As a result, Kodak revised the useful lives of certain existing production machinery and equipment, and manufacturing-related buildings

effective January 1, 2011. These assets, many of which were previously set to fully depreciate by 2012 to 2013, were changed to depreciate with

estimated useful lives ending from 2012 to

63