IHOP 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

56

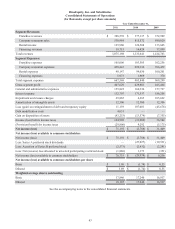

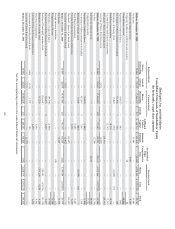

At December 31, 2011, the Company had a liability for unrecognized tax benefit including potential interest and penalties,

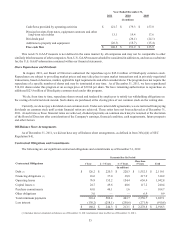

net of related tax benefit, totaling $8.9 million, of which approximately $2.0 million is expected to be paid within one year. For

the remaining liability, due to the uncertainties related to these tax matters, the Company is unable to make a reasonably reliable

estimate when a cash settlement with a taxing authority will occur. This liability is included in "Other obligations" above.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance with U.S. GAAP requires us to make estimates and assumptions that

affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of net revenues

and expenses in the reporting period. We base our estimates and assumptions on current facts, historical experience and various

other factors that we believe to be reasonable under the circumstances, the results of which form the basis for making judgments

about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other

sources. Accounting assumptions and estimates are inherently uncertain and actual results may differ materially from our estimates.

We believe the following critical accounting policies require us to make significant judgments and estimates in the preparation

of our consolidated financial statements:

Goodwill and Intangibles

Goodwill is recorded when the aggregate purchase price of an acquisition exceeds the estimated fair value of the net identified

tangible and intangible assets acquired. Intangible assets resulting from the acquisition are accounted for using the purchase method

of accounting and are estimated by management based on the fair value of the assets received. Identifiable intangible assets are

comprised primarily of trademarks, tradenames, liquor licenses, which are considered to have an indefinite life, and franchise

agreements, recipes and menus and favorable lease agreements, which are considered to have a finite life. Intangible assets with

finite lives are being amortized over the period of estimated benefit using the straight-line method and estimated useful lives.

Goodwill and indefinite life intangible assets are not subject to amortization.

Goodwill has been allocated to three reporting units, the IHOP unit, Applebee's company unit and Applebee's franchise unit.

The significant majority of the Company's goodwill resulted from the November 29, 2007 acquisition of Applebee's and has been

allocated between the two Applebee's units. The goodwill allocated to the Applebee's company unit was fully impaired in 2008.

The Company tests goodwill and other indefinite life intangible assets for impairment on an annual basis in the fourth quarter.

The annual impairment test of goodwill of the Applebee's franchise unit is performed as of October 31 of each year. The annual

impairment test of the goodwill of the IHOP unit is performed as of December 31 of each year, the date as of which the analysis

has been performed in prior years. In addition to the annual test of impairment, goodwill and indefinite life intangible assets must

be evaluated more frequently if the Company believes indicators of impairment exist. Such indicators include, but are not limited

to, events or circumstances such as a significant adverse change in the business climate, unanticipated competition, a loss of key

personnel, adverse legal or regulatory developments, or a significant decline in the market price of the Company's common stock.

In the process of the Company's annual impairment review of goodwill, the Company primarily uses the income approach

method of valuation that includes the discounted cash flow method as well as other generally accepted valuation methodologies

to determine the fair value. Significant assumptions used to determine fair value under the discounted cash flows model include

future trends in sales, operating expenses, overhead expenses, depreciation, capital expenditures, and changes in working capital

along with an appropriate discount rate. Additional assumptions are made as to proceeds to be received from future refranchising

of company-operated restaurants. Step one of the impairment test compares the fair value of each of our reporting units to its

carrying value. If the fair value is in excess of the carrying value, no impairment exists. If the step one test does indicate an

impairment, step two must take place. Under step two, the fair value of the assets and liabilities of the reporting unit are estimated

as if the reporting unit were acquired in a business combination. The excess of the fair value of the reporting unit over the carrying

amounts assigned to its assets and liabilities is the implied fair value of the goodwill, to which the carrying value of the goodwill

must be adjusted. The fair value of all reporting units is then compared to the current market value of the Company's common

stock to determine if the fair values estimated in the impairment testing process are reasonable in light of the current market value.

In the process of the Company's annual impairment review of the tradename, the most significant indefinite life intangible

asset, the Company primarily uses the relief of royalty method under the income approach method of valuation. Significant

assumptions used to determine fair value under the relief of royalty method include future trends in sales, a royalty rate and a

discount rate to be applied to the forecasted revenue stream.

Long-Lived Assets

We assess long-lived and intangible assets with finite lives for impairment when events or changes in circumstances indicate

that the carrying value of the assets may not be recoverable. We test impairment using historical cash flows and other relevant