IHOP 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

49

Tradename Impairment

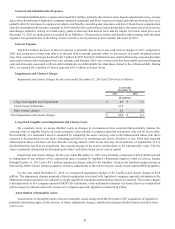

In accordance with U.S. GAAP, indefinite-lived intangible assets must be evaluated for impairment, at a minimum, on an

annual basis, and more frequently if we believe indicators of impairment exist. Such indicators include, but are not limited to,

events or circumstances such as a significant adverse change in the business climate, unanticipated competition, a loss of key

personnel, adverse legal or regulatory developments, or a significant decline in the market price of our common stock. In performing

the impairment review of the tradename intangible asset, we primarily use the relief of royalty method under the income approach

method of valuation. Significant assumptions used to determine fair value under the relief of royalty method include future trends

in sales, a royalty rate and a discount rate to be applied to the forecast revenue stream. During the course of fiscal 2010 and 2009,

we made periodic assessments as to whether there were indicators of impairment, particularly with respect to the significant

assumptions noted above. As a result of these assessments, we determined an interim test of indefinite-lived intangibles was not

necessary in either 2010 or 2009.

During the fourth quarter of 2010, we performed the annual test of impairment for indefinite-lived intangibles, primarily

the Applebee's tradename assigned in the purchase price allocation. We determined the estimated fair value of our indefinite-lived

intangible assets exceeded the carrying values and in the absence of other indicators of impairment we concluded no impairment

was necessary. During the fourth quarter of 2009, we performed the annual test of impairment for indefinite-lived intangibles. As

the result of the test, the estimated fair value of the tradename was less than the carrying value and an impairment of $93.5 million

was recognized, along with a related tax benefit of $37.2 million.

Long-lived Tangible Asset Impairment and Closure Costs

On a quarterly basis, we assess whether events or changes in circumstances have occurred that potentially indicate the

carrying value of tangible long-lived assets, primarily assets related to company-operated restaurants, may not be recoverable.

Recoverability of a restaurant's assets is measured by comparing the assets' carrying value to the undiscounted future cash flows

expected to be generated over the assets' remaining useful lives or remaining lease terms, whichever is less. If the total expected

undiscounted future cash flows are less than the carrying amount of the assets, this may be an indicator of impairment. If it is

decided that there has been an impairment, the carrying amount of the asset is written down to the estimated fair value. The fair

value is primarily determined by discounting the future cash flows based on our cost of capital.

As the result of performing these assessments throughout 2010, we recognized impairments of long-lived tangible assets of

$1.5 million. In October 2010, we sold 63 company-operated Applebee's restaurants located in Minnesota and Wisconsin. We had

fee ownership of the properties on which three of the restaurants were located. Our strategy does not contemplate retaining such

properties as a lessor on a long-term basis. The properties were transferred to assets held for sale and an impairment of $0.7 million

was recorded based on the estimated sales price. We also placed a single restaurant and the land on which it is situated up for sale.

In accordance with criteria under U.S. GAAP we transferred the fair value of the assets related to this restaurant, as determined

by the estimated sales price, to assets held for sale and an impairment of $0.5 million was recognized. Other minor impairments

totaled $0.3 million.

Closure charges in 2010 of $2.0 million related primarily to two company-operated IHOP Cafe restaurants (a non-traditional

restaurant test format that was evaluated but will no longer be utilized) and to the closure of a company-operated Applebee's

restaurant in China.

As the result of performing these assessments throughout 2009, we recognized impairments of long-lived tangible assets of

$10.4 million in 2009. The impaired assets comprised three IHOP company-operated restaurants, various assets related to one

IHOP franchise restaurant, one Applebee's company-operated restaurant, a write-down to the estimated sales value based on a

current letter of intent of one Applebee's restaurant that had been closed in a prior period and included in assets held for sale as

of December 31, 2008 and four parcels of Applebee's real estate. We had fee ownership of the properties on which four Applebee's

company-operated restaurants were located. These restaurants were refranchised in the fourth quarter of 2008 but we retained

ownership of the land and continued to lease the property to the franchisee. Our strategy does not contemplate retaining such

properties as a lessor on a long-term basis. During the third quarter of 2009, we determined the properties met the requirements

under U.S. GAAP to be reclassified as assets held for sale. The properties were written down to the estimated fair value that will

be received upon sale. We evaluated the causal factors of all impairments of long-lived assets as they were recorded during 2010

and 2009 and concluded they were based on factors specific to each asset and were not potential indicators of an impairment of

goodwill, indefinite-lived intangible assets or other long-lived assets. Closure costs of $1.2 million related to two IHOP franchise

restaurants.

Loss/Gain on Extinguishment of Debt and Temporary Equity

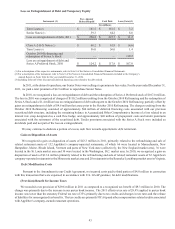

In 2010, we recognized a loss on extinguishment of debt and temporary equity of $107.0 million compared with a gain on

extinguishment of debt of $45.7 million in 2009. The loss in 2010 was comprised of charges of $110.2 million resulting from the

October 2010 Refinancing and the redemption of Series A Stock and a $1.4 million loss on extinguishment of debt subsequent to