IHOP 2011 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2011 IHOP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

52

We may in the future enter into hedging agreements to mitigate the effect of changes in LIBOR on variable interest rates.

Mandatory Repayments

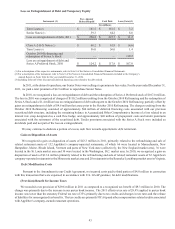

Loans under the Credit Agreement are subject to the following repayment requirements:

• 1% per year of principal balance (the mandatory repayment is based upon the $742.0 million New Term Loan);

• 50% of excess cash flow (as defined in the Credit Agreement), paid, at a minimum, on an annual basis; and

• 100% of asset sales and insurance proceeds (subject to certain exclusions).

We may voluntarily prepay loans under both the Term Facility and the Revolving Facility without premium or penalty.

However, if we make a voluntary prepayment within one year after the closing date of the Credit Agreement in the case of the

Revolving Facility, or one year after the February 2011 Refinancing in the case of the Term Facility, in connection with any

transaction that results in a lower effective interest rate, we must pay a prepayment premium in an amount equal to 1.0% of the

principal amount prepaid, as applicable. There were no prepayment premiums required during 2011.

There are no mandatory repayments of the Senior Notes, although under certain conditions we may be required to repurchase

Senior Notes with excess proceeds of assets sales or upon a change of control, as described in the Indenture under which the Senior

Notes were issued.

Based on our current level of operations, we believe that our cash flow from operations, available cash and available

borrowings under our Revolving Facility will be adequate to meet our liquidity needs during 2012.

Debt Covenants

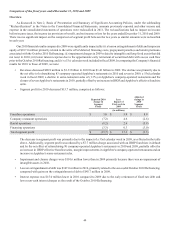

Pursuant to the Credit Agreement we are required to comply with a maximum consolidated leverage ratio and a minimum

consolidated cash interest coverage ratio. The Company's current required maximum consolidated leverage ratio of total debt (net

of unrestricted cash not to exceed $75 million) to adjusted EBITDA is 7.5x. Our current required minimum ratio of adjusted

EBITDA to consolidated cash interest is 1.5x. Compliance with each of these ratios is required quarterly, on a trailing four-quarter

basis. These ratio thresholds become more rigorous over time. The maximum consolidated leverage ratio will decline, in annual

25-basis-point decrements beginning with the first quarter of 2012, to 6.5x by the first quarter of 2015, then to 6.0x for the first

quarter of 2016 until the Credit Agreement expires in October 2017. The minimum consolidated cash interest coverage ratio will

increase to 1.75x commencing in the first quarter of 2013 and to 2.0x commencing in the first quarter of 2016 and remain at that

level until the Credit agreement expires in October 2017.

For the trailing twelve months ended December 31, 2011, our consolidated leverage ratio was 5.3x and our consolidated

cash interest coverage ratio was 2.3x.

There are no financial maintenance covenants associated with the Senior Notes.

The Senior Notes, the Term Facility and the Revolving Facility are also subject to affirmative and negative covenants

considered customary for similar types of facilities, including, but not limited to, covenants with respect to incremental indebtedness,

liens, restricted payments (including dividends), investments, affiliate transactions, and capital expenditures. These covenants are

subject to a number of important limitations, qualifications and exceptions. Importantly, certain of these covenants will not be

applicable to the Notes during any time that the Notes maintain investment grade ratings.

The EBITDA used in calculating these ratios is considered to be a non-U.S. GAAP measure. The reconciliation between

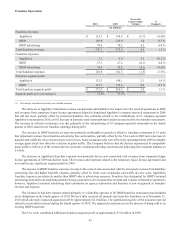

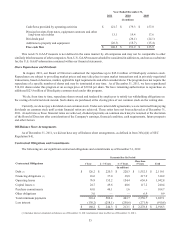

our income before income taxes, as determined in accordance with U.S. GAAP, and EBITDA used for covenant compliance

purposes is as follows: