HSBC 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

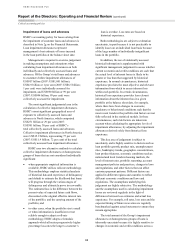

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

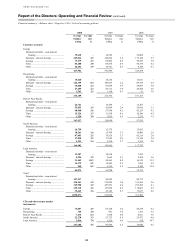

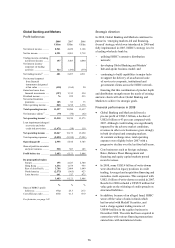

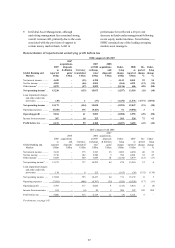

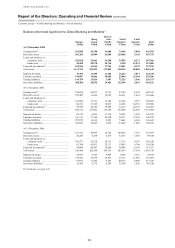

Customer groups > Personal Financial Services

70

Subsequent developments

The branch-based US consumer lending business of

HSBC Finance has historically focused on sub-prime

customers who rely on drawing cash against the

equity in their homes to help meet their cash needs.

Unsecured consumer lines of credit have served as a

means of generating new customer accounts, with

the potential to subsequently provide the customer

with a mortgage product, typically a secured debt

consolidation loan. As a result, the bulk of the

mortgage lending products sold in the US consumer

lending branch network have been for refinancing

and debt consolidation rather than for house

purchase.

The unprecedented deterioration in the US

housing market over the last two years, including

declining property values and lower secondary

market demand for sub-prime mortgages, has

undermined the ability of many real estate loan

customers to make payments or refinance their loans.

In many cases, there is no equity in their homes or, if

there is, few institutions are willing to finance its

withdrawal. As a result, loan originations in this

business have fallen dramatically for both HSBC

Finance and the industry as a whole. Management

believes it will take years before property values

return to the levels seen prior to the decline and, as

such, has concluded that recovery in the sub-prime

mortgage lending business is uncertain and the

industry is unlikely to stabilise for a number of

years. Management also expects that changes in

regulation and practice will make it problematic to

plan and execute a sub-prime lending business

strategy with a reasonable degree of confidence.

Given the above, in 2008 HSBC began to

reposition its US consumer lending business to

reduce risk by tightening lending criteria and

expanding its lending to include government

sponsored entity and conforming loan products. As

part of this repositioning, HSBC intended to place

greater emphasis on unsecured loan products while

decreasing secured loan production. To date, the

results of this repositioning effort have not met

expectations, in part due to the continued

deterioration in the economy, leading management to

re-evaluate whether, given the Group’s risk appetite,

the initiative can produce the volume necessary to

ensure that the consumer lending business will return

to profitability in the foreseeable future.

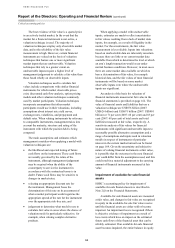

As a consequence, at the end of February 2009,

the Board of HSBC endorsed management’s

recommendation to discontinue as soon as

practicable originations of all products by the

branch-based US consumer lending business of

HSBC Finance. At 31 December 2008 this business

had outstanding balances of US$62 billion

comprising US$46 billion in real estate secured and

US$16 billion in unsecured loan balances. HSBC

will continue to service and collect the existing loan

portfolio as it runs off, and will continue the Group’s

efforts to help customers in need of loan

modification and other account management

programmes to maximise collection and preserve, as

far as possible, home ownership. In the US,

substantially all consumer lending branches branded

HFC and Beneficial will cease taking loan

applications and will be closed. HSBC Finance will

also continue to run-off the loan portfolios of its

mortgage services business and its vehicle finance

business. HSBC will provide all necessary support to

HSBC Finance to enable it to run off these

businesses in a measured way and to meet all its

commitments.

The operations of HSBC’s other US Personal

Financial Services businesses, including its card

business, and the retail bank branch business of

HSBC USA are unaffected by this decision. HSBC

USA will continue to service its customers with real

estate secured and unsecured products.

HSBC expects as a result of this decision

affecting the US consumer lending business of

HSBC Finance that total revenue will fall by

approximately US$50 million in 2009 and operating

expenses by approximately US$700 million on an

annualised basis. Closure costs of up to

US$195 million will be incurred, predominantly

related to one-off termination and other employee

benefit costs, a substantial portion of which will be

recorded in the first half of 2009.

In addition, a non-cash charge of approximately

US$70 million is expected to be incurred in relation

to the impairment of fixed assets associated with the

consumer lending branch network, also to be

recognised in the first half of 2009.

Employees supporting originations operations

will be evaluated for service elsewhere in HSBC’s

operations, but it is currently expected that

approximately 6,100 employees will be displaced.