HSBC 2008 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

101

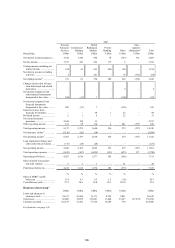

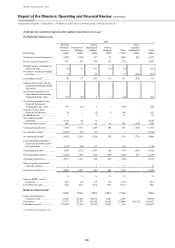

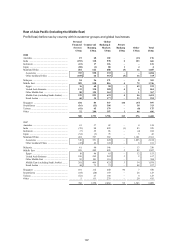

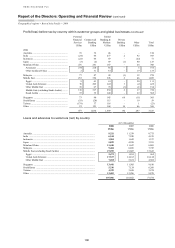

of trade finance grew strongly, driven by demand

from corporates with international trade

requirements, and commercial lending balances rose,

particularly during the first half of the year.

Fee income declined by 23 per cent, driven by

lower equity market-related revenues. Weak market

sentiment led to lower volumes of retail brokerage

and a decrease in income from wealth management

activity. This was partly offset by a rise in fees from

cards following increases in both cards in circulation

and cardholder spending. Fees from account services

rose due to greater customer activity and there were

higher fees generated from bundled products.

Trading income was 4 per cent lower, driven by

further write-downs of US$0.2 billion in Global

Banking and Markets on a legacy monoline

exposure. Excluding these write-downs, trading

income grew due to a rise in foreign exchange and

rates income as continuing market volatility

generated increased trading opportunities and

demand for active hedging products.

The net loss of US$1.2 billion on financial

instruments designated at fair value compared with

income of US$676 million in 2007. The loss

reflected a decline in the value of assets linked to the

insurance business. To a large extent, these losses

are attributable to policyholders, with an equivalent

reduction in net insurance claims and movement in

liabilities to policyholders. While the decline in the

value of assets which relate to unit-linked products is

allocated to policyholders in full, the portion of

decline in the value passed on to clients who have

products with discretionary participation features

and guarantees may be restricted.

Losses from financial investments of

US$309 million reflected impairments required on

investments which have experienced significant falls

in equity market prices. These equity investments

are classified as available for sale, are not held for

trading, and remain part of the strategic positioning

of HSBC’s businesses in Asia. These losses

were partly offset by an aggregate gain of

US$203 million from the redemption of shares

in the Visa initial public offering (‘IPO’) and the

disposal of MasterCard shares.

Net earned insurance premiums increased by

16 per cent to US$3.2 billion, largely due to growth

in the life insurance business, in particular for

policies with discretionary participation features.

Net insurance claims and movement in

liabilities to policyholders fell by 40 per cent,

reflecting the decline in asset values noted above

partly offset by increases due to growth in

premiums.

Loan impairment charges and other credit risk

provisions rose markedly from the previously low

level to US$765 million as economic conditions

deteriorated. Within these charges were exposures to

financial institutions held within Global Banking and

Markets, which resulted in other credit risk

provisions. In Commercial Banking, the combination

of an absence of significant recoveries recorded in

2007 and weakness among certain exporters in Hong

Kong, who were affected by reduced demand from

the US and other developed countries, raised loan

impairment charges. As local businesses responded

to the economic environment, unemployment rose in

the second half of 2008. Credit policies were

consequently adjusted across certain products as

delinquency and bankruptcy increased in

Hong Kong. Although property market declines

reduced equity levels for residential mortgage

customers, the impact on loan impairment charges

was limited as this lending was well-secured and

regulatory restrictions constrained origination loan-

to-value ratios to below 70 per cent.

Operating expenses rose by 4 per cent. Staff

costs declined by 3 per cent despite wage increases

and a rise in the number of customer-facing staff,

largely due to lower performance-related costs in

Global Banking and Markets. Staff numbers were

higher than in 2007 notwithstanding reductions

within the branch network for lower business

volumes in the latter part of 2008. IT costs rose as

investment in systems continued. Marketing costs

were lower following active management of costs

while property rental costs increased due to higher

market rental rates. Overall, cost growth was

curtailed in response to the more difficult economic

climate.

2007 compared with 2006

Economic briefing

Hong Kong’s economy remained robust during

2007, with the annual rate of growth of 6.3 per cent.

Domestic consumption was the major contributor to

economic expansion, supported by the strong labour

market. The unemployment rate fell to 3.4 per cent, a

nine year low, as the supply of labour remained very

tight. Global increases in food and oil prices affected

Hong Kong, but the territory also experienced wage

inflation, rising import prices and growth in property

rental costs. Inflation increased as a result, exceeding

3 per cent in the final quarter of the year.

In response to interest rate cuts in the US and

capital inflows into the local market, Hong Kong’s