HSBC 2008 Annual Report Download - page 246

Download and view the complete annual report

Please find page 246 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

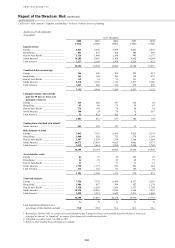

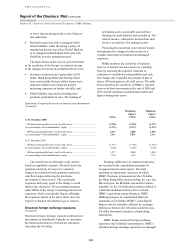

Market risk > Trading portfolios / Non-trading portfolios

244

Trading portfolios

(Audited)

HSBC’s control of market risk is based on a policy

of restricting individual operations to trading within

a list of permissible instruments authorised for each

site by Traded Credit and Market Risk, of enforcing

rigorous new product approval procedures, and of

restricting trading in the more complex derivative

products only to offices with appropriate levels of

product expertise and robust control systems.

Market making and proprietary position taking

is undertaken within Global Markets. The VAR for

such trading activity at 31 December 2008 was

US$72.5 million (2007: US$30.2 million). This is

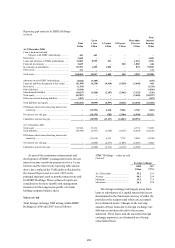

analysed below by risk type:

VAR by risk type for the trading activities (excluding Credit Spread VAR)

(Audited)

Foreign

exchange and

commodity

Interest

rate

Equity Total1

US$m US$m US$m US$m

At 31 December 2008 .................................................. 29.8 63.4 13.9 72.5

At 31 December 20072 .................................................. 10.7 25.4 10.2 30.2

Average

2008 .......................................................................... 19.0 50.7 15.2 53.1

20072 ......................................................................... 9.5 22.9 7.9 23.7

Minimum

2008 .......................................................................... 8.7 21.4 8.2 22.6

20072 ......................................................................... 4.0 14.9 3.4 14.3

Maximum

2008 .......................................................................... 54.9 147.4 39.0 104.4

20072 ......................................................................... 23.0 36.1 15.1 38.8

1 The total VAR is non-additive across risk types due to diversification effects.

2 The VAR for 2007 has been adjusted on the same basis as Group VAR on page 243.

Credit spread risk

The risk associated with movements in credit

spreads is primarily managed through sensitivity

limits, stress testing, and VAR for those portfolios

where VAR is calculated.

The Group is introducing credit spread as a

separate risk type within the VAR models. At

31 December 2008, credit spread VAR was

calculated for the London trading and New York

credit derivatives portfolios. At that date, the total

VAR for the trading activities, including credit

spread VAR for the above portfolios, was

US$106.4 million (2007: US$43.8 million)

compared with a total VAR of US$72.5 million

reported within the ‘VAR by risk type for the

trading activities’ (see above), which excludes the

credit spread VAR for these two portfolios.

The sensitivity of trading income to the effect

of movements in credit spreads on the total trading

activities of the Group was US$590.9 million at

31 December 2008 (2007: US$95.4 million). This

sensitivity captures the credit spread exposure

arising from positions taken throughout the Group,

in addition to the London trading and New York

credit derivative portfolios captured within credit

spread VAR (see above). The sensitivity was

calculated using simplified assumptions based on

one-day movements in average market credit spreads

over a two-year period at a confidence level of

99 per cent, and assumes a simultaneous movement

in credit spreads across issuers. It should be noted

that diversification effects within the portfolio and

with other risk types is likely to lead to a reduced

impact on trading income.

The significant increase in the sensitivity at

31 December 2008, compared with 31 December

2007, was due to the effect of much higher volatility

in credit spreads observed during 2008. The actual

positions within the trading portfolios exposed to

credit spread risk were lower on 31 December 2008

than on 31 December 2007.

In addition to the above measure certain

portfolios are also managed using default risk

measures where appropriate.

The measurement of the credit spread impact on

trading income as at 31 December 2008 excludes

those positions that were reclassified as non-trading

during the second half of 2008 following the

amendment to IFRS. These positions are included

within the 31 December 2007 comparative, as the

reclassification took effect from 1 July 2008.

Credit spread risk also arises on credit derivative

transactions entered into by Global Banking in order

to manage the risk concentrations within the

corporate loan portfolio and so enhance capital