HSBC 2008 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

17

Increased regulation of the financial services

industry could have an adverse effect on

HSBC’s operations

HSBC, its subsidiaries and its affiliates are subject to

extensive and increasing regulation, accounting

standards and interpretations thereof and legislation

in the various countries in which the Group operates.

From time to time, new laws are introduced,

including tax, consumer protection, privacy and

other legislation, which affect the operating

environment in which the Group operates. As a

result of the recent interventions by governments in

response to global economic conditions, it is widely

expected that there will be a substantial increase in

government regulation and supervision of the

financial services industry, including the imposition

of higher capital requirements and restrictions on

certain types of transaction structure. If enacted,

such new regulations could require additional capital

to be injected into HSBC’s subsidiaries and

affiliates, require HSBC to enter into business

transactions that are not otherwise part of its current

Group strategy, prevent HSBC from continuing

current lines of operations, restrict the type or

volume of transactions HSBC may enter into, limit

HSBC’s subsidiaries’ and affiliates’ ability to declare

dividends to HSBC, or set limits on or require the

modification of rates or fees that HSBC charges on

certain loan or other products. HSBC may also face

increased compliance costs and limitations on its

ability to pursue business opportunities. Separately,

the Basel II Accord’s requirement for financial

institutions to increase their capital in response to

deteriorating market conditions may have secondary

effects on lending, which could exacerbate the

current market downturn. These measures, alone or

in combination, could have an adverse effect on

HSBC’s operations.

In the UK for example, the Banking Act 2009

includes a ‘Special Resolutions Regime’ which gives

wide powers in respect of UK banks and their parent

companies to the UK Treasury, the FSA and the

Bank of England in circumstances where any such

UK bank has encountered, or is likely to encounter,

financial difficulties.

HSBC is subject to tax-related risks in the

countries in which it operates, which could

have an adverse effect on its operating

results

HSBC is subject to the substance and interpretation

of tax laws in all countries in which it operates.

A number of double taxation agreements entered into

between countries also affect the taxation of the

Group. Tax risk is the risk associated with changes

in tax law or in the interpretation of tax law. It also

includes the risk of changes in tax rates and the risk

of consequences arising from failure to comply with

procedures required by tax authorities. Failure to

manage tax risks could lead to increased tax charges,

including financial or operating penalties, for not

complying as required with tax laws.

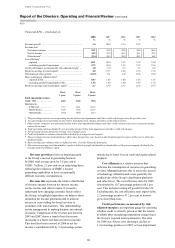

Key performance indicators

The Board of Directors and the Group Management

Board monitor HSBC’s progress against its strategic

objectives. Progress is assessed by comparison with

the Group’s strategy, its operating plan targets and its

historical performance using both financial and non-

financial measures.

As a prerequisite for the vesting of Performance

Shares, the Remuneration Committee must satisfy

itself that HSBC Holdings’ financial performance

has shown a sustained improvement in the period

since the award date. In determining this, the

Remuneration Committee will take account of all

relevant factors but in particular comparisons against

the total shareholder return (‘TSR’) comparator

group with regard to the financial key performance

indicators (‘KPIs’) described below.

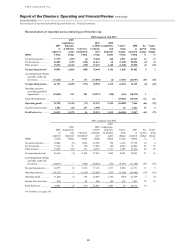

Financial KPIs

To support the Group’s strategy and ensure that

HSBC’s performance can be monitored,

management utilises a number of financial KPIs. The

table below presents these KPIs for the period from

2004 to 2008. At a business level, the KPIs are

complemented by a range of benchmarks which are

relevant to the planning process and to reviewing

business performance.

HSBC has published a number of key targets

against which future performance can be measured.

Financial targets have been set as follows: the return

on average total shareholders’ equity over the

medium term has been set at 15-19 per cent; the cost

efficiency ratio has been set in the range of 48-52 per

cent; and the TSR in the top half of that achieved by

peers. The cost efficiency ratio has been set as a

range within which the business is expected to

remain in order to accommodate the need for

continued investment in support of future business

growth.