HSBC 2008 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

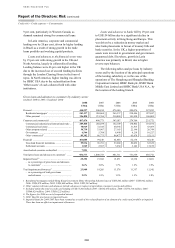

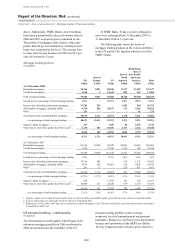

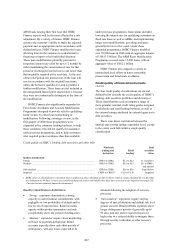

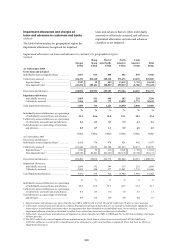

Credit risk > Areas of special interest > US personal lending / Loan delinquency in US

214

Second lien loans have a risk profile

characterised by higher loan-to-value ratios because,

in many cases, the second lien loan was taken out to

complete the refinancing or purchase of the property.

For HSBC Finance second lien mortgages, the

proportion of customers two months or more behind

on contractual payments rose from 11.2 per cent at

31 December 2007 to 15.9 per cent at 31 December

2008. Loss on default of second lien loans typically

approaches 100 per cent of the amount owed as any

equity in the property is applied initially to the first

lien loan, particularly during periods of house price

depreciation when its value is eroded to the point

where there is no surplus available to support the

repayment of second liens.

Stated-income mortgages, which represented a

small part of the HSBC Finance loan book, also

continued to decline. These mortgages are of higher

than average risk as they are underwritten on the

basis of borrowers’ representations of annual income

and are not verified by receipt of supporting

documentation. These loan balances declined

from US$8.3 billion at 31 December 2007 to

US$5.7 billion at 31 December 2008. Two months or

more delinquency rates on stated-income loans rose

from 19.0 per cent at 31 December 2007 to 27.7 per

cent at 31 December 2008. The percentage rise was

primarily attributable to lower balances and portfolio

ageing as the portfolio continued to run off.

In the Mortgage Services business, credit quality

continued to deteriorate as 2005 and 2006 vintages

continued to season and move into later stages of

delinquency as economic conditions worsened.

Amounts of two months or more delinquency in

Mortgage Services rose by 9 per cent during the year

to US$4.7 billion at 31 December 2008. These

represented an increased proportion of a reducing

portfolio, rising from 11.9 per cent to 17.0 per cent.

An increase in foreclosures in process during the

fourth quarter, arising from a voluntary one month

suspension of final court proceedings in foreclosure

cases relating to owner occupied properties,

implemented in December 2008 and the actions

taken by a number of states to slow foreclosure

proceedings, affected total lending in Mortgage

Services at 31 December 2008.

HSBC undertook several actions during 2008 to

reposition HSBC Finance, including closure of more

than 200 consumer lending branches, reducing the

network to approximately 800 branches, and

tightening credit criteria for originations. These

actions followed the decisions taken in 2007 to

cease purchasing mortgages from third-party

correspondents and to close the wholesale business,

Decision One, in September 2007, thereby ending

new originations for the Mortgage Services business.

The branch-based consumer lending business

continued to experience rising delinquency levels,

particularly on first lien loans in the states most

exposed to falling house prices and rising

unemployment; 63 per cent of the increase in

amounts of two months or more contractual

delinquency was concentrated in the ten states noted

above. Delinquencies rose across all vintages, with

the most pronounced increase for first lien loans

extended in 2006 and 2007. This trend was

experienced across the rest of the industry in the US.

Two months or more delinquencies rose from 4.2 per

cent of loans and advances at 31 December 2007 to

12.1 per cent at 31 December 2008 and delinquent

balances increased to US$5.6 billion. In this

environment, HSBC took additional measures to

tighten underwriting standards, including reducing

the loan to value ratio for residential mortgages,

ceasing to underwrite certain products and raising

the credit requirements for certain risk factors. As a

result, originations declined to 38 per cent of the

levels recorded in 2007.

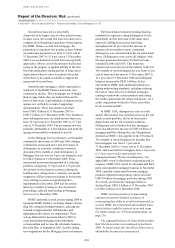

At HSBC USA, delinquencies rose as credit

quality deterioration was experienced across the real

estate secured portfolio, driven by house price

depreciation and the US economic weakness.

Delinquency rates of prime first lien mortgages

were also affected by the sale of US$7.0 billion of

mortgage portfolios during the year. Originations

declined as HSBC’s risk appetite in the US reduced.

Two months or more delinquencies in prime first

lien mortgages rose from 1.1 per cent at

31 December 2007 to 3.4 per cent at 31 December

2008, and in second lien mortgages from 1.8 per cent

to 3.5 per cent over the same period, on a

management basis. The rise in delinquency was

appreciably worse in third-party originations and, in

response, HSBC USA closed its wholesale and third-

party correspondent mortgage business in November

2008, curtailed certain stated-income mortgage

products, tightened underwriting criteria and sold

US$7.0 billion of mortgage portfolios during 2008.

As a result, stated-income mortgage balances

declined from US$2.4 billion at 31 December 2007

to US$2.2 billion at 31 December 2008.

HSBC has been proactive in approaching

customers to provide financial assistance in

restructuring their debts to avoid foreclosure and, as

a result, HSBC has restructured and modified loans

that it believes could be serviced on revised terms.

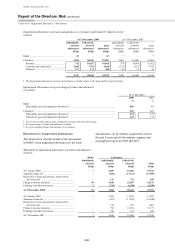

For further details, see ‘US loan modifications’ on

page 216.

The aggregate balances of loans which reached

their first interest rate reset continued to decline in

2008. As interest rates fall, the effect of the reset on

affordability becomes less pronounced.