HSBC 2008 Annual Report Download - page 279

Download and view the complete annual report

Please find page 279 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

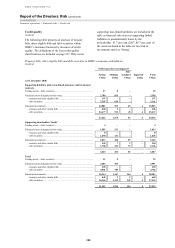

277

reporting, leaving a small residue of exposures on

the standardised approach.

Market risk is derived from fluctuations on

trading book assets arising from changes in values,

income, interest and foreign exchange rates and is

measured using VAR models with FSA permission

or the standard rules prescribed by the FSA.

Counterparty credit risk in the trading book and the

non-trading book is the risk that the counterparty to a

transaction may default before completing the

satisfactory settlement of the transaction. Three

counterparty credit risk calculation approaches are

defined by Basel II to determine exposure values,

being the standardised, mark to market and the

internal model method. These exposure values are

then used to determine capital requirements using

one of the credit risk approaches, standardised, IRB

foundation and IRB advanced. Across the Group,

HSBC uses both VAR and standard rules approaches

for market risk and the mark to market and internal

model method approaches for counterparty credit

risk. It is the longer-term aim of HSBC to migrate

more positions from standard rules to VAR for

market risk and from mark to market to internal

model method for counterparty credit risk.

Basel II also introduces capital requirements for

operational risk and, again, contains three levels of

sophistication. The capital required under the basic

indicator approach is a simple percentage of gross

revenues, whereas under the standardised approach it

is one of three different percentages of gross

revenues allocated to each of eight defined business

lines. Both these approaches use an average of the

last three financial years’ revenues. Finally, the

advanced measurement approach uses banks’ own

statistical analysis and modelling of operational risk

data to determine capital requirements. HSBC has

adopted the standardised approach to the

determination of Group operational risk capital

requirements.

The second pillar of Basel II (Supervisory

Review and Evaluation Process – ‘SREP’) involves

both firms and regulators taking a view on whether a

firm should hold additional capital against risks not

covered in pillar 1. Part of the pillar 2 process is the

Internal Capital Adequacy Assessment Process

(‘ICAAP’) which is the firm’s self assessment of the

levels of capital that it needs to hold. The pillar 2

process culminates in the FSA providing firms with

Individual Capital Guidance (‘ICG’). The ICG

replaces the trigger ratio and is set as a capital

resources requirement higher than that required

under pillar 1.

Pillar 3 of Basel II is related to market discipline

and aims to make firms more transparent by

requiring them to publish specific, prescribed details

of their risks, capital and risk management under the

Basel II framework. On 10 November 2008, HSBC

published summary qualitative pillar 3 disclosures

(‘Interim Pillar 3 Disclosures 2008’) for 30 June

2008 on the investor relations section of its website,

www.hsbc.com. HSBC expects to publish the first

full set of pillar 3 disclosures for 31 December 2008,

including quantitative tables, during the first half of

2009.

During 2007, HSBC was supervised under

Basel I. Under Basel I, banking operations are

categorised as either trading book or banking book

and risk-weighted assets are determined accordingly.

Banking book risk-weighted assets are measured by

means of a hierarchy of risk weightings classified

according to the nature of each asset and

counterparty, taking into account any eligible

collateral or guarantees. Banking book off-balance

sheet items giving rise to credit, foreign exchange or

interest rate risk are assigned weights appropriate to

the category of the counterparty, taking into account

any eligible collateral or guarantees. Trading book

risk-weighted assets are determined by taking into

account market-related risks such as foreign

exchange, interest rate and equity position risks, and

counterparty risk.