HSBC 2008 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

213

decline of 19 per cent in 2008). These factors

restricted the ability of many customers to refinance

and access equity retained in their homes.

Two months or more delinquencies in

mortgages originated through the HSBC Finance

branch network rose most rapidly in those states

most severely affected by continued house price

depreciation and rising unemployment, particularly

in California, Florida, New York, Virginia,

Maryland, New Jersey, Illinois, Pennsylvania,

Massachusetts and Ohio.

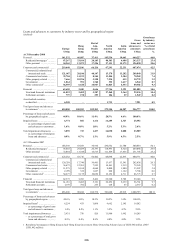

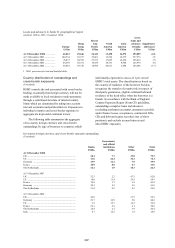

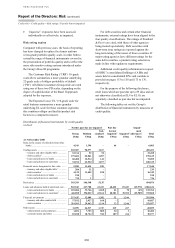

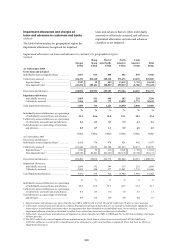

HSBC Finance: geographical concentration of US lending1,2

(Unaudited)

Mortgage lending as a

percentage of:

Other personal lending as a

percentage of:

total

lending

total

mortgage

lending

total

lending

total other

personal

lending

Percentage

of total

lending

% % % % %

California ............................................................................... 6 11 6 12 12

Florida .................................................................................... 4 7 3 7 7

New York ............................................................................... 3 6 3 6 6

Texas ...................................................................................... 2 3 4 8 6

Ohio ....................................................................................... 3 5 2 5 5

Pennsylvania .......................................................................... 3 5 2 5 5

1 By states which individually account for 5 per cent or more of HSBC Finance’s US customer loan portfolio.

2 HSBC Finance lending is shown on a management basis and includes loans transferred to HSBC USA Inc, which are managed by

HSBC Finance.

In the US real estate secured portfolios, two

months and over contractual delinquency ratios at

the end of 2008 were higher across the portfolio

than during 2007 and the first half of 2008, for

the reasons described above. There was also a

significant effect on delinquency ratios from

declining balances. As the portfolios aged,

outstanding balances fell as new lending in certain

portfolios ceased, risk mitigation efforts and changes

to product offerings which began in 2007 and

continued in 2008 resulted in lower originations

and US$8.2 billion in mortgage portfolios were

sold during the year.

Both dollar and percentage two months and over

contractual delinquency in the real estate secured

portfolios of HSBC Finance and HSBC USA

increased following a voluntary one month

suspension of final court proceedings in foreclosure

cases relating to owner-occupied properties,

implemented in December 2008, which was in

addition to actions taken by a number of states to

slow foreclosure proceedings. Within these

portfolios, dollar delinquencies rose sharply in 2008

as credit quality in the consumer lending portfolio,

most notably for first lien products, and in Mortgage

Services, continued to deteriorate, particularly in the

second half of the year. In Mortgage Services, the

rise in the fourth quarter of 2008 was despite lower

balances following portfolio run-off and the sale of

portfolios during the year, and was partly caused by

the above-mentioned action on foreclosure.

Residential mortgages

The unprecedented turmoil in the mortgage lending

market continued in 2008. Investors remained

unwilling to purchase securitised credit, and this

resulted in a sharp contraction in the supply of

liquidity to the mortgage market. Progressively

fewer refinancing options were available for

customers as house prices fell and housing equity

declined, a number of market participants exited the

sub-prime mortgage industry, and the remaining

providers tightened their underwriting criteria.

Equity withdrawal had been the principal source

of credit available to sub-prime borrowers dealing

with unforeseen financial needs. With this source of

funds heavily restricted, consumers faced increasing

difficulty in maintaining their contractual payment

schedules as they confronted the challenges of rising

unemployment and increases in the costs of living,

particularly in the first half of the year.

Compounding the situation, mortgage interest rates

remained high for much of 2008 as credit spreads on

interbank lending widened due to the turmoil in the

global financial system.

The increase in delinquency rates was

accompanied by a rise in loss severities as falling

house prices led to a reduction in the amounts

recoverable from foreclosure and repossession.

These factors were partly offset by a decline in

lending balances as HSBC continued to manage

down exposure in the US.