HSBC 2008 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

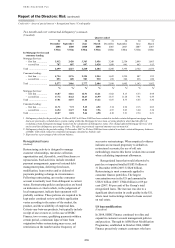

Credit risk > Areas of special interest > Renegotiated loans // Credit quality

216

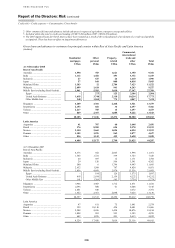

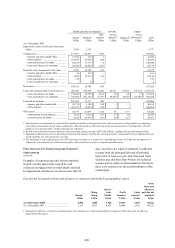

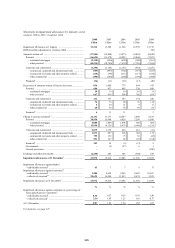

Two months and over contractual delinquency1 (continued)

(Unaudited)

Quarter ended

31

December

2008

30

September

2008

30

June

2008

31

March

2008

31

December

2007

30

September

2007

30

June

2007

31

March

2007

US$m US$m US$m US$m US$m US$m US$m US$m

In Mortgage Services and

consumer lending

Mortgage Services:

– first lien ................. 3,912 3,420 3,363 3,456 3,248 2,554 2,099 1,863

– second lien ............. 787 807 897 1,028 1,050 841 663 613

Total ............................... 4,699 4,227 4,260 4,484 4,298 3,395 2,762 2,476

Consumer lending:

– first lien ................. 4,724 3,176 2,194 1,954 1,622 1,259 907 832

– second lien ............. 853 690 583 530 478 346 236 220

Total ............................... 5,577 3,866 2,777 2,484 2,100 1,605 1,143 1,052

%

3 %3 %

3 %

3 %

3 %

3 %3 %3

Mortgage Services:

– first lien ................. 16.87 14.16 12.91 12.41 11.02 8.13 6.33 4.98

– second lien ............. 17.72 16.62 16.63 16.99 15.57 11.28 7.91 6.59

Total ............................... 17.01 14.57 13.55 13.22 11.87 8.73 6.65 5.30

Consumer lending:

– first lien ................. 11.71 7.72 5.15 4.52 3.74 2.92 2.15 2.03

– second lien ............. 14.54 11.27 9.04 7.96 6.97 5.03 3.60 3.34

Total ............................... 12.07 8.18 5.66 4.98 4.18 3.21 2.34 2.21

1 Delinquency data for the period from 31 March 2007 to 30 June 2008 has been restated to include certain delinquent mortgage loans

that were previously excluded due to system coding within the Mortgage Services loan servicing platform which had the effect of

excluding certain delinquent mortgage loans from the calculation of delinquency ratios. This change affected Mortgage Services’ first

and second lien delinquency percentages above. The effect on previously reported amounts was not material.

2 Delinquency data for the periods ending 31 December 2007 to 30 June 2008 has been restated to exclude certain delinquency balances

of HSBC USA which related to residential mortgages classified as held for sale.

3 Expressed as a percentage of the relevant balance.

Renegotiated loans

(Audited)

Restructuring activity is designed to manage

customer relationships, maximise collection

opportunities and, if possible, avoid foreclosure or

repossession. Such activities include extended

payment arrangements, approved external debt

management plans, deferring foreclosure,

modification, loan rewrites and/or deferral of

payments pending a change in circumstances.

Following restructuring, an overdue consumer

account is normally reset from delinquent to current

status. Restructuring policies and practices are based

on indicators or criteria which, in the judgement of

local management, indicate that repayment will

probably continue. These policies are required to be

kept under continual review and their application

varies according to the nature of the market, the

product, and the availability of empirical data.

Criteria vary between products, but typically include

receipt of one or more or, in the case of HSBC

Finance, two or more, qualifying payments within a

certain period, a minimum lapse of time from

origination before restructuring may occur, and

restrictions on the number and/or frequency of

successive restructurings. When empirical evidence

indicates an increased propensity to default on

restructured accounts, the use of roll rate

methodology ensures this factor is taken into account

when calculating impairment allowances.

Renegotiated loans that would otherwise be

past due or impaired totalled US$35 billion at

31 December 2008 (2007: US$28 billion).

Restructuring is most commonly applied to

consumer finance portfolios. The largest

concentration was in the US and amounted to

US$31 billion (2007: US$24 billion) or 89 per

cent (2007: 86 per cent) of the Group’s total

renegotiated loans. The increase was due to a

significant deterioration in credit quality in the US,

where most restructurings related to loans secured

on real estate.

US loan modifications

(Unaudited)

In 2008, HSBC Finance continued to refine and

expand its customer account management policies

and practices. Through its ARM Reset Modification

Programme, established in October 2006, HSBC

Finance proactively contacts customers who have