HSBC 2008 Annual Report Download - page 233

Download and view the complete annual report

Please find page 233 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

231

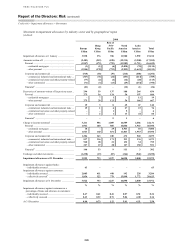

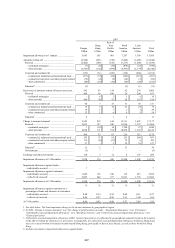

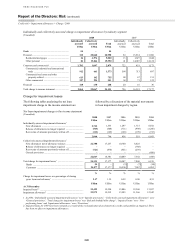

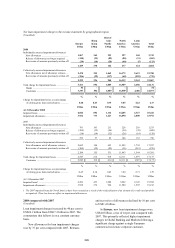

commentary that follows is on a constant currency

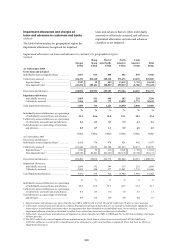

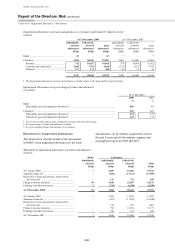

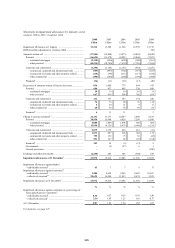

basis:

New allowances for loan impairment charges

rose by 52 per cent, compared with 2006. Releases

and recoveries of allowances increased by 1 per cent

to US$1.6 billion.

In Europe, new loan impairment charges were

US$3.5 billion, a rise of 8 per cent compared with

2006. This partly reflected growth in commercial

lending, where charges remained low compared with

historical amounts but rose from the exceptionally

low levels experienced in 2005 and 2006. Increased

charges also reflected growth in credit card lending

in Turkey. In the UK, refinements to the

methodology used to calculate roll rate percentages

resulted in a higher charge in the consumer finance

operations in the first half of the year. Excluding

this, loan impairment charges were marginally lower

than in 2006.

Releases and recoveries in Europe were broadly

in line with 2006.

In Hong Kong, new loan impairment charges of

US$287 million were recorded, an increase of 19 per

cent, due to the growth in credit card balances and

new corporate loan charges.

Releases and recoveries in Hong Kong

decreased to US$75 million, primarily in the

corporate sector. This reflected the low level of

allowances added in recent years.

In Rest of Asia-Pacific, new loan impairment

charges rose by 10 per cent to US$834 million, with

higher loan impairment charges arising in the

commercial loan books in Thailand and Malaysia.

This was offset by a decline in loan impairment

charges for personal lending, particularly in Taiwan

and Indonesia, where charges returned to more

regular levels after an upsurge in 2006 due to

regulatory changes which affected collection activity

and minimum payments.

With corporate and commercial loan impairment

charges low in recent years, releases and recoveries

decreased by 6 per cent to US$220 million.

New loan impairment charges in North America

rose by 76 per cent to US$12.2 billion, driven by the

continued deterioration in credit quality in the US

consumer finance loan portfolio.

US credit quality deteriorated as mortgage

delinquencies rose, house prices declined,

refinancing credit became less available in the

market and the macroeconomic outlook worsened.

Other factors affecting the rise in US loan

impairment charges included normal seasoning of

the portfolio, a higher proportion of unsecured

personal lending and a return to historical norms

from the unusually low levels of bankruptcy filings

experienced in 2006, following changes enacted to

US bankruptcy law in 2005.

Delinquency rates rose across all parts of the

HSBC Finance personal lending portfolio, with

Mortgage Services and consumer lending

experiencing significant rises in delinquency which

flowed through subsequent stages through to

foreclosure. As the housing downturn began to have

more effect on the broader economy, delinquency

rates in credit cards and vehicle finance rose in the

final quarter of 2007. A change in product mix in the

cards portfolio towards higher yielding products also

contributed to higher impairment charges as this

segment of the portfolio seasoned.

Releases and recoveries in North America

decreased to US$116 million. In the US consumer

finance business, collection staff increased in all

lending portfolios as part of the response to the

deteriorating credit environment.

In Latin America, new loan impairment

charges rose by 63 per cent to US$2.0 billion. The

most significant increase was registered in Mexico,

reflecting strong growth in balances, normal

portfolio seasoning and a rise in delinquency rates

in credit cards. Charges for commercial lending in

Mexico fell as increased delinquency rates in the

small and medium-sized business portfolios were

offset by impairment allowance releases. Products

with high credit losses were discontinued or

restructured. Loan impairment charges in Brazil rose

marginally, due to growth in store loans and credit

cards.

Releases and recoveries in Latin America

increased to US$272 million. In Brazil, credit

models were changed during 2007 to align with

credit behaviour in underlying portfolios.