Burger King 2006 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2006 Burger King annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

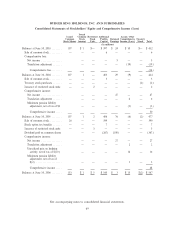

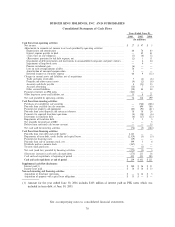

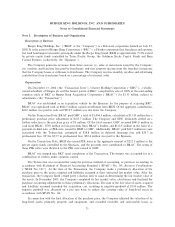

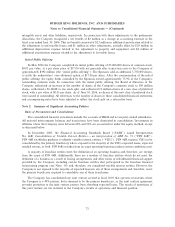

BURGER KING HOLDINGS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements Ì (Continued)

advertising, marketing and related activities, and result in no gross profit recognized by the Company.

Amounts which are contributed to the advertising funds by company owned restaurants are recorded as

selling, general and administrative expenses. Advertising expense, net of franchisee contributions, totaled

$74 million for the year ended June 30, 2006, $87 million for the year ended June 30, 2005, and $100 million

for the year ended June 30, 2004 and is included in selling, general and administrative expenses.

To the extent that contributions received exceed advertising and promotional expenditures, the excess

contributions are accounted for as deferred credits, in accordance with SFAS No. 45, and are recorded in

accrued advertising in the accompanying consolidated balance sheets.

Franchisees in markets where no Company-owned restaurants operate contribute to advertising funds not

managed by the Company. Such contributions and related fund expenditures are not reflected in the

Company's results of operations or financial position.

Income Taxes

The Company files a consolidated U.S. federal income tax return. Amounts in the financial statements

related to income taxes are calculated using the principles of SFAS No. 109, Accounting for Income Taxes

(""SFAS No. 109''). Under SFAS No. 109, deferred tax assets and liabilities reflect the impact of temporary

differences between the amounts of assets and liabilities recognized for financial reporting purposes and the

amounts recognized for tax purposes, as well as tax credit carryforwards and loss carryforwards. These

deferred taxes are measured by applying currently enacted tax rates. The effects of changes in tax rates on

deferred tax assets and liabilities are recognized in income in the year in which the law is enacted. A valuation

allowance reduces deferred tax assets when it is ""more likely than not'' that some portion or all of the deferred

tax assets will not be recognized.

Earnings per Share

Basic earnings per share is computed by dividing net income attributable to common stockholders by the

weighted average number of common shares outstanding for the period. The computation of diluted earnings

per share is consistent with that of basic earnings per share, while giving effect to all dilutive potential common

shares that were outstanding during the period.

Stock-based Compensation

The Company accounts for stock-based compensation using the intrinsic-value method in accordance

with Accounting Principles Board Opinion (""APB'') No. 25, Accounting for Stock Issued to Employees

(""APB No. 25''), and related interpretations. Pro forma information regarding net income and earnings per

share is required by SFAS No. 123, Accounting for Stock Based Compensation (""SFAS No. 123''). In

estimating the fair value of its options under SFAS No. 123, the Company uses the minimum value method.

In addition, the Company will adopt SFAS 123(R), Share-Based Payment, (""SFAS 123(R)'') on July 1,

2006. As such, the Company became a public company, as the term is defined in SFAS 123(R), on

February 16, 2006, the date the Company filed its S-1 registration statement with the SEC in anticipation of

its initial public offering of common stock, which was completed in May 2006. In accordance with

SFAS 123(R), the Company is required to apply the modified prospective transition method to any share-

based payments issued subsequent to the filing of the registration statement; however no stock compensation

cost will begin to be recognized for such awards in the financial statements until the Company adopts

SFAS 123(R) on July 1, 2006. As a result, the pro-forma information regarding net income and earnings per

share required by SFAS 123 would also include an estimated volatility factor for those share-based payment

awards issued for the period February 16, 2006 to June 30, 2006. However, the amount of stock compensation

for these awards was immaterial, therefore, the following assumptions for the Black-Scholes model are only

those used to calculate compensation cost using the minimum value method.

77