Burger King 2006 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2006 Burger King annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

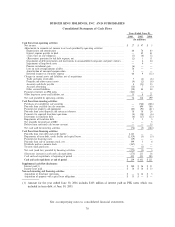

|

|

underlying exposures. Our policies prohibit the use of derivative instruments for trading purposes, and we have

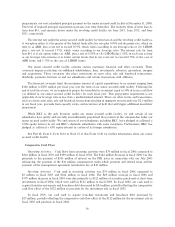

procedures in place to monitor and control their use.

Foreign Currency Exchange Risk

Movements in foreign currency exchange rates may affect the translated value of our earnings and cash

flow associated with our foreign operations, as well as the translation of net asset or liability positions that are

denominated in foreign countries. In countries outside of the United States where we operate company

restaurants, we generate revenues and incur operating expenses and selling, general and administrative

expenses denominated in local currencies. In many foreign countries where we do not have Company

restaurants our franchisees pay royalties in U.S. dollars. However, as the royalties are calculated based on local

currency sales, our revenues are still impacted from fluctuations in exchange rates. In fiscal 2006, operating

income would have decreased or increased $9.5 million if all foreign currencies uniformly weakened or

strengthened 10% relative to the U.S. dollar.

We use derivative instruments to reduce the foreign exchange impact on earnings from changes in the

value of foreign-denominated assets and liabilities. At June 30, 2006, we had forward currency contracts

outstanding to sell Euros, British Pounds and Canadian dollars totaling $346 million, $27 million and

$5 million, respectively, to hedge intercompany notes and offset the foreign exchange risk associated with the

remeasurement of these notes. Changes in the fair value of these forward contracts due to changes in the spot

rate between the U.S. dollar and the Euro, British Pound and Canadian dollar are offset by the remeasurement

of the intercompany notes resulting in insignificant impact to the Company's net income. The contracts

outstanding at June 30, 2006 mature at various dates through October 2006 and we intend to continue to

renew these contracts to hedge our foreign exchange impact.

Interest Rate Risk

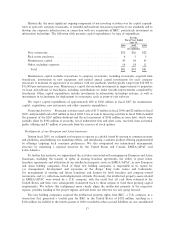

We have a market risk exposure to changes in interest rates, principally in the United States. We attempt

to minimize this risk and lower our overall borrowing costs through the utilization of derivative financial

instruments, primarily interest rate swaps. These swaps are entered into with financial institutions and have

reset dates and critical terms that match those of the underlying debt. Accordingly, any change in market

value associated with interest rate swaps is offset by the opposite market impact on the related debt.

During the year ended June 30, 2006, we entered into interest rate swaps with a notional value of

$750 million that qualify as cash flow hedges under SFAS No. 133, Accounting for Derivative Instruments and

Hedging Activities. The interest rate swaps help us manage exposure to interest rate risk by converting the

floating interest-rate component of approximately 75% of our total debt obligations outstanding at June 30,

2006 to fixed rates. A 1% change in interest rates on our existing debt of $998 million would result in an

increase or decrease in interest expense of approximately $2.5 million in a given year, as we have hedged

$750 million of our debt.

Commodity Price Risk

We purchase certain products, particularly beef, which are subject to price volatility that is caused by

weather, market conditions and other factors that are not considered predictable or within our control.

Additionally, our ability to recover increased costs is typically limited by the competitive environment in

which we operate. We do not utilize commodity option or future contracts to hedge commodity prices and do

not have long-term pricing arrangements. As a result, we purchase beef and other commodities at market

prices, which fluctuate on a daily basis.

The estimated change in company restaurant food, paper and product costs from a hypothetical 10%

change in average beef prices would have been approximately $9 million and $8 million in fiscal 2006 and

fiscal 2005, respectively. The hypothetical change in food, paper and product costs could be positively or

negatively affected by changes in prices or product sales mix.

64