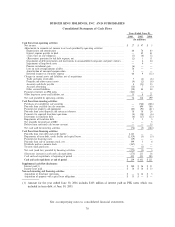

Burger King 2006 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2006 Burger King annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

No. 25, Accounting for Stock Issued to Employees (""APB No. 25''). SFAS No. 123(R) requires all share-

based payments to employees, including grants of employee stock options, to be recognized in the income

statement based on their fair values. Pro forma disclosure is no longer an alternative. Under

SFAS No. 123(R) the effective date for a nonpublic entity that becomes a public entity after June 15, 2005 is

the first interim or annual reporting period beginning after becoming a public company. Further,

SFAS No. 123(R) states that an entity that makes a filing with a regulatory agency in preparation for the sale

of any class of equity securities in a public market is considered a public entity for purposes of

SFAS No. 123(R). We implemented SFAS No. 123(R) effective July 1, 2006.

As permitted by SFAS No. 123, for periods prior to July 1, 2006 we accounted for share-based payments

to employees using APB No. 25's intrinsic value method and, as such, generally recognized no compensation

expense for employee stock options. As we currently apply SFAS No. 123 pro forma disclosure using the

minimum value method of accounting, we are required to adopt SFAS No. 123(R) using the prospective

transition method. Under the prospective transition method, non-public entities that previously applied

SFAS No. 123 using the minimum value method continue to account for non-vested awards outstanding at

the date of adoption of SFAS No. 123(R) in the same manner as they had been accounted to prior to

adoption. For us, since we accounted for our equity awards using the minimum value method under APB

No. 25, we will continue to apply APB No. 25 to equity awards outstanding at the date we adopt

SFAS No. 123(R), and as a result not recognize compensation expense for awards issued prior to the date we

filed our Registration Statement on Form S-1 in February 2006.

From the date of the filing of our initial Registration Statement in February 2006, we are required to

apply the modified prospective transition method to any share-based payments issued subsequent to the filing

of the registration statement but prior to the effective date of our adoption of SFAS No. 123(R). Under the

modified prospective transition method, compensation expense is recognized for any unvested portion of the

awards granted between filing date and adoption date of SFAS No. 123(R) over the remaining vesting period

of the awards beginning on the adoption date, for us July 1, 2006.

For any awards granted subsequent to the adoption of SFAS No. 123(R), compensation expense will be

recognized over the service period of the award, based on the fair value at the grant date. The impact of the

adoption of this statement on the Company in fiscal 2007 and beyond will depend on various factors including,

but not limited to, our future stock-based compensation grants. We currently estimate the adoption of

SFAS 123(R) will decrease net income by approximately $3 million for fiscal 2007.

In June 2006, the FASB issued FASB Interpretation No. 48, Accounting for Uncertainty in Income Taxes

(""FIN 48''). FIN 48 clarifies the accounting for uncertainty in income taxes recognized in an enterprise's financial

statements in accordance with SFAS No. 109. FIN 48 prescribes a recognition threshold and measurement

attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in

a tax return. The evaluation of a tax position in accordance with FIN 48 is a two-step process. The first step is to

determine whether it is more-likely-than-not that a tax position will be sustained upon examination based on the

technical merits of the position. The second step is measurement of any tax position that meets the more-likely-

than-not recognition threshold to determine the amount of benefit to recognize in the financial statements. The tax

position is measured at the largest amount of benefit that is greater than 50 percent likely of being realized upon

ultimate settlement. An enterprise that presents a classified statement of financial position should classify a liability

for unrecognized tax benefits as current to the extent that the enterprise anticipates making a payment within one

year or the operating cycle. FIN 48 is effective for fiscal years beginning after December 15, 2006. We are

currently evaluating the impact that FIN 48 may have on our statements of operations and statements of financial

position when we adopt FIN 48 on July 1, 2007.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

Market Risk

We are exposed to financial market risks associated with foreign currency exchange rates, interest rates

and commodity prices. In the normal course of business and in accordance with our policies, we manage these

risks through a variety of strategies, which may include the use of derivative financial instruments to hedge our

63