Allstate 2014 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2014 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

periods as a result of their incidence of occurrence and magnitude, and can have a significant impact on the combined

ratio. Prior year reserve reestimates are caused by unexpected loss development on historical reserves. Business

combination expenses and the amortization of purchased intangible assets relate to the acquisition purchase price and

are not indicative of our underlying insurance business results or trends. We believe it is useful for investors to evaluate

these components separately and in the aggregate when reviewing our underwriting performance. We also provide it to

facilitate a comparison to our outlook on the underlying combined ratio. The most directly comparable GAAP measure

is the combined ratio. The underlying combined ratio should not be considered a substitute for the combined ratio and

does not reflect the overall underwriting profitability of our business.

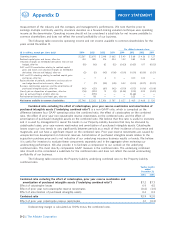

The following table reconciles the Property-Liability underlying combined ratio to the Property-Liability combined ratio

for the years ended December 31.

2014 2013 2012 2011 2010

Underlying combined ratio 87.2 87.3 87.2 89.3 89.6

Effect of catastrophe losses 6.9 4.5 8.8 14.7 8.5

Effect of prior year non-catastrophe reserve reestimates (0.4) (0.1) (1.0) (0.8) —

Effect of business combination expenses and the amortization of purchased intangible

assets 0.2 0.3 0.5 0.2 —

Combined ratio 93.9 92.0 95.5 103.4 98.1

Underwriting margin is calculated as 100% minus the combined ratio.

Operating income return on common shareholders’ equity is a ratio that uses a non-GAAP measure. It is calculated by

dividing the rolling 12-month operating income by the average of common shareholders’ equity at the beginning and at

the end of the 12-months, after excluding the effect of unrealized net capital gains and losses. Return on common

shareholders’ equity is the most directly comparable GAAP measure. We use operating income as the numerator for the

same reasons we use operating income, as discussed above. We use average common shareholders’ equity excluding

the effect of unrealized net capital gains and losses for the denominator as a representation of common shareholders’

equity primarily attributable to the company’s earned and realized business operations because it eliminates the effect

of items that are unrealized and vary significantly between periods due to external economic developments such as

capital market conditions like changes in equity prices and interest rates, the amount and timing of which are unrelated

to the insurance underwriting process. We use it to supplement our evaluation of net income available to common

shareholders and return on common shareholders’ equity because it excludes the effect of items that tend to be highly

variable from period to period. We believe that this measure is useful to investors and that it provides a valuable tool for

investors when considered along with return on common shareholders’ equity because it eliminates the after-tax effects

of realized and unrealized net capital gains and losses that can fluctuate significantly from period to period and that are

driven by economic developments, the magnitude and timing of which are generally not influenced by management. In

addition, it eliminates non-recurring items that are not indicative of our ongoing business or economic trends. A

byproduct of excluding the items noted above to determine operating income return on common shareholders’ equity

from return on common shareholders’ equity is the transparency and understanding of their significance to return on

common shareholders’ equity variability and profitability while recognizing these or similar items may recur