Allstate 2014 Annual Report Download - page 265

Download and view the complete annual report

Please find page 265 of the 2014 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

-

277

-

278

-

279

-

280

|

|

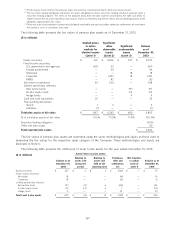

Weighted average assumptions used to determine benefit obligations as of December 31 are listed in the following

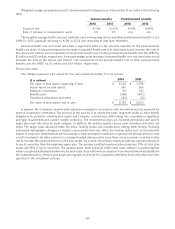

table.

Pension benefits Postretirement benefits

2014 2013 2014 2013

Discount rate 4.10% 5.00% 4.15% 4.85%

Rate of increase in compensation levels 3.5 3.5 n/a n/a

The weighted average health care cost trend rate used in measuring the accumulated postretirement benefit cost is

6.8% for 2015, gradually declining to 4.5% in 2024 and remaining at that level thereafter.

Assumed health care cost trend rates have a significant effect on the amounts reported for the postretirement

health care plans. A one percentage-point increase in assumed health care cost trend rates would increase the total of

the service and interest cost components of net periodic benefit cost of other postretirement benefits and the APBO by

$2 million and $25 million, respectively. A one percentage-point decrease in assumed health care cost trend rates would

decrease the total of the service and interest cost components of net periodic benefit cost of other postretirement

benefits and the APBO by $2 million and $24 million, respectively.

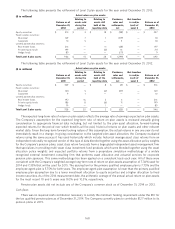

Pension plan assets

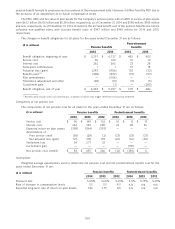

The change in pension plan assets for the years ended December 31 is as follows:

2014 2013

($ in millions)

Fair value of plan assets, beginning of year $ 5,602 $ 5,398

Actual return on plan assets 540 566

Employer contribution 49 561

Benefits paid (368) (892)

Translation adjustment and other (40) (31)

Fair value of plan assets, end of year $ 5,783 $ 5,602

In general, the Company’s pension plan assets are managed in accordance with investment policies approved by

pension investment committees. The purpose of the policies is to ensure the plans’ long-term ability to meet benefit

obligations by prudently investing plan assets and Company contributions, while taking into consideration regulatory

and legal requirements and current market conditions. The investment policies are reviewed periodically and specify

target plan asset allocation by asset category. In addition, the policies specify various asset allocation and other risk

limits. The target asset allocation takes the plans’ funding status into consideration, among other factors, including

anticipated demographic changes or liquidity requirements that may affect the funding status such as the potential

impact of lump sum settlements as well as existing or expected market conditions. In general, the allocation has a lower

overall investment risk when a plan is in a stronger funded status position since there is less economic incentive to take

risk to increase the expected returns on the plan assets. As a result, the primary employee plan has a greater allocation

to equity securities than the employee-agent plan. The primary qualified employee plan comprises 79% of total plan

assets and 81% of equity securities. The pension plans’ asset exposure within each asset category is tracked against

widely accepted established benchmarks for each asset class with limits on variation from the benchmark established in

the investment policy. Pension plan assets are regularly monitored for compliance with these limits and other risk limits

specified in the investment policies.

165