Allstate 2014 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2014 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

freeze losses not meeting our criteria to be declared a catastrophe), are accrued on an occurrence basis within the policy

period. Therefore, in any reporting period, loss experience from catastrophic events and weather-related losses may

contribute to negative or positive underwriting performance relative to the expectations we incorporated into the

products’ pricing. We pursue rate increases where indicated, taking into consideration potential customer disruption,

the impact on our ability to market our auto lines, regulatory limitations, our competitive position and profitability, using

a methodology that appropriately addresses the changing costs of losses from catastrophes such as severe weather and

the net cost of reinsurance.

Allstate Protection outlook

• Allstate Protection will continue to focus on its strategy of offering differentiated products and services to our

customers while maintaining pricing discipline.

• We expect that volatility in the level of catastrophes we experience will contribute to variation in our

underwriting results; however, this volatility will be mitigated due to our catastrophe management actions,

including the purchase of reinsurance.

• We will continue our evolution to a trusted advisor model, enabling agencies to more fully deliver on the

Allstate brand customer value proposition.

• We will continue to modernize our operating model to efficiently deliver our customer value propositions.

• We will invest in building long-term growth platforms.

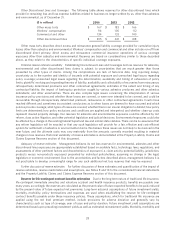

Premiums written is the amount of premiums charged for policies issued during a fiscal period. Premiums are

considered earned and are included in the financial results on a pro-rata basis over the policy period. The portion of

premiums written applicable to the unexpired term of the policies is recorded as unearned premiums on our

Consolidated Statements of Financial Position.

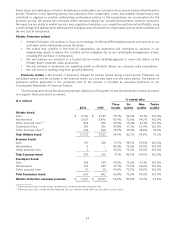

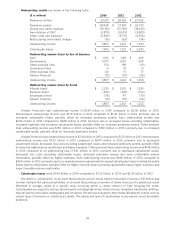

The following table shows the unearned premium balance as of December 31 and the timeframe in which we expect

to recognize these premiums as earned.

% earned after

($ in millions)

Three Six Nine Twelve

2014 2013 months months months months

Allstate brand:

Auto $ 4,766 $ 4,533 70.7% 96.2% 99.1% 100.0%

Homeowners 3,607 3,496 43.4% 75.5% 94.2% 100.0%

Other personal lines (1) 833 819 43.5% 75.4% 94.1% 100.0%

Commercial lines 254 236 43.8% 75.1% 93.9% 100.0%

Other business lines (2) 642 468 18.9% 33.3% 45.4% 55.3%

Total Allstate brand 10,102 9,552 54.9% 82.7% 93.4% 97.2%

Esurance brand:

Auto 371 328 73.7% 98.5% 99.6% 100.0%

Homeowners 6 — 43.4% 75.6% 94.2% 100.0%

Other personal lines 2 1 43.5% 75.4% 94.2% 100.0%

Total Esurance brand 379 329 73.1% 98.0% 99.5% 100.0%

Encompass brand:

Auto 345 335 43.8% 75.6% 94.1% 100.0%

Homeowners 274 253 43.7% 75.7% 94.2% 100.0%

Other personal lines 57 54 43.9% 75.7% 94.2% 100.0%

Total Encompass brand 676 642 43.8% 75.6% 94.2% 100.0%

Allstate Protection unearned premiums $ 11,157 $ 10,523 54.8% 82.8% 93.7% 97.4%

(1) Other personal lines include renter, condominium, landlord and other personal lines.

(2) Other business lines include Allstate Roadside Services, Allstate Dealer Services and other business lines.

34