AT&T Wireless 2015 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2015 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

|

|

AT&T INC.

|

71

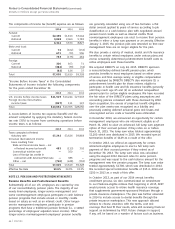

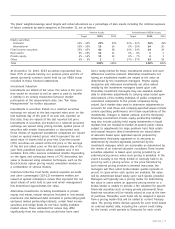

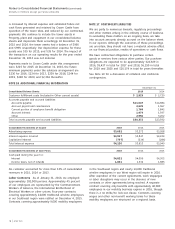

The plans’ weighted-average asset targets and actual allocations as a percentage of plan assets, including the notional exposure

of future contracts by asset categories at December 31, are as follows:

Pension Assets Postretirement (VEBA) Assets

Target 2015 2014 Target 2015 2014

Equity securities:

Domestic 20% – 30% 22% 23% 21% – 31% 26% 29%

International 10% – 20% 15 14 9% – 19% 14 20

Fixed income securities 35% – 45% 40 38 29% – 39% 34 29

Real assets 6% – 16% 10 11 0% – 6% 1 1

Private equity 4% – 14% 12 12 0% – 7% 2 3

Other 0% – 5% 1 2 17% – 27% 23 18

Total 100% 100% 100% 100%

had a ready market for these investments existed, and such

differences could be material. Alternative investments not

having an established market are valued at fair value as

determined by the investment managers. Private equity,

mezzanine and distressed investments are often valued

initially by the investment managers based upon cost.

Thereafter, investment managers may use available market

data to determine adjustments to carrying value based upon

observations of the trading multiples of public companies

considered comparable to the private companies being

valued. Such market data used to determine adjustments to

accounts for cash flows and company-specified issues include

current operating performance and future expectations of the

investments, changes in market outlook, and the third-party

financing environment. Private equity partnership holdings

may also include publicly held equity investments in liquid

markets that are marked-to-market at quoted public values,

subject to adjustments for large positions held. Real estate

and natural resource direct investments are valued either

at amounts based upon appraisal reports prepared by

independent third-party appraisers or at amounts as

determined by internal appraisals performed by the

investment manager, which are reasonable as determined by

the review of an external valuation consultant. Fixed income

securities valuation is based upon pricing provided by an

external pricing service when such pricing is available. In the

event a security is too thinly traded or narrowly held to be

priced by such a pricing service, or the price furnished by

such external pricing services is deemed inaccurate, the

managers will then solicit broker/dealer quotes (spreads or

prices). In cases where such quotes are available, fair value

will be determined based solely upon such quotes provided.

Managers will typically use a pricing matrix for determining

fair value in cases where an approved pricing service or a

broker/dealer is unable to provide a fair valuation for specific

fixed-rate securities such as many private placements. New

fixed-rate securities will be initially valued at cost at the time

of purchase. Thereafter, each bond will be assigned a spread

from a pricing matrix that will be added to current Treasury

rates. The pricing matrix derives spreads for each bond based

on external market data, including the current credit rating

for the bonds, credit spreads to Treasuries for each credit

At December 31, 2015, AT&T securities represented less

than 0.5% of assets held by our pension plans and 6% of

assets (primarily common stock) held by our VEBA trusts

included in these financial statements.

Investment Valuation

Investments are stated at fair value. Fair value is the price

that would be received to sell an asset or paid to transfer

a liability in an orderly transaction between market

participants at the measurement date. See “Fair Value

Measurements” for further discussion.

Investments in securities traded on a national securities

exchange are valued at the last reported sales price on the

last business day of the year. If no sale was reported on

that date, they are valued at the last reported bid price.

Investments in securities not traded on a national securities

exchange are valued using pricing models, quoted prices of

securities with similar characteristics or discounted cash

flows. Shares of registered investment companies are valued

based on quoted market prices, which represent the net

asset value of shares held at year-end. Over-the-counter

(OTC) securities are valued at the bid price or the average

of the bid and asked price on the last business day of the

year from published sources where available and, if not

available, from other sources considered reliable. Depending

on the types and contractual terms of OTC derivatives, fair

value is measured using valuation techniques, such as the

Black-Scholes option pricing model, simulation models or

a combination of various models.

Common/collective trust funds, pooled separate accounts

and other commingled (103-12) investment entities are

valued at quoted redemption values that represent the net

asset values of units held at year-end which management

has determined approximates fair value.

Alternative investments, including investments in private

equity, real estate, natural resources (included in real assets),

mezzanine and distressed debt (included in partnerships/joint

ventures), limited partnership interests, certain fixed income

securities and hedge funds do not have readily available

market values. These estimated fair values may differ

significantly from the values that would have been used