Singapore Airlines 2007 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2007 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

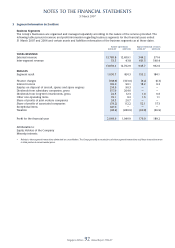

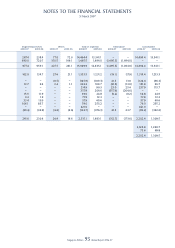

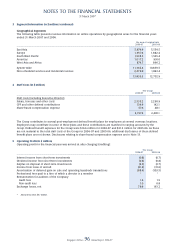

Singapore Airlines 89 Annual Report 2006-07

NOTES TO THE FINANCIAL STATEMENTS

31 March 2007

2 Accounting Policies (continued)

(aa)

Capitalised loan interest

Borrowing costs incurred to fi nance progress payments for aircraft and building projects are capitalised until the

aircraft are commissioned for operation or the projects are completed. All other borrowing costs are recognised as

expenses in the period in which they are incurred.

(

ab

)

Impairment of non-fi nancial and fi nancial assets

An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s fair value less costs to sell and

its value in use and is determined for an individual asset, unless the asset does not generate cash infl ows that are

largely independent of those from other assets or groups of assets.

The carrying amounts of the Group’s non-fi nancial assets are reviewed at each balance sheet date to determine

whether there is any indication of impairment. An impairment loss is recognised whenever the carrying amount

of an asset exceeds its recoverable amount. The impairment loss is charged to the profi t and loss account unless

it reverses a previous revaluation credited to equity, in which case it is charged to equity. An impairment loss is

reversed if there has been a change in estimates used to determine the recoverable amount.

The Group also assesses at each balance sheet date whether a fi nancial asset or a group of fi nancial assets is

impaired.

(i) Assets carried at amortised cost

If there is objective evidence that an impairment loss on loans and receivables carried at amortised cost has

been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and

the present value of estimated future cash fl ows (excluding future credit losses that have not been incurred)

discounted at the fi nancial asset’s original effective interest rate. The carrying amount of the asset shall be

reduced either directly or through use of an amortisation account. The amount of the loss shall be recognised in

the profi t and loss account.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related

objectively to an event occurring after the impairment was recognised, the previously recognised impairment

is reversed. Any subsequent reversals of an impairment loss is recognised in the profi t and loss account, to the

extent that the carrying value of the asset does not exceed its amortised cost at the reversal date.

(ii) Assets carried at cost

If there is objective evidence that an impairment loss on an unquoted equity instrument that is not carried at fair

value because its fair value cannot be reliably measured, the amount of the loss is measured as the difference

between the asset’s carrying amount and the estimated realisable amount. Such impairment losses are not

reversed in subsequent periods.

(iii) Available-for-sale fi nancial assets

If an available-for-sale asset is impaired, an amount comprising the difference between its cost and its current

fair value, less any impairment loss previously recognised in profi t and loss account, is transferred from equity

to the profi t and loss account. Reversals in respect of equity instruments classifi ed as available-for-sale are not

recognised in the profi t and loss account. Reversals of impairment losses on debt instruments are reversed

through the profi t and loss account, if the increase in fair value of the instrument can be objectively related to an

event occurring after the impairment loss was recognised in the profi t and loss account.

(ac)

Derivative fi nancial instruments and hedging

The Group uses derivative fi nancial instruments such as forward currency contracts, interest rate swap contracts, jet

fuel options and jet fuel swap contracts to hedge its risks associated with foreign currency, interest rate and jet fuel

price fl uctuations. Such derivative fi nancial instruments are initially recognised at fair value on the date on which a

derivative contract is entered into, and are subsequently re-measured at fair value. Derivatives are carried as assets

when the fair value is positive, and as liabilities when the fair value is negative.

Any gains or losses arising from changes in fair value on derivatives that do not qualify for hedge accounting are

taken directly to the profi t and loss account.