Singapore Airlines 2007 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2007 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

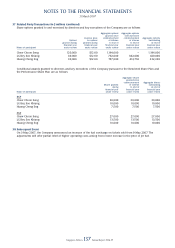

NOTES TO THE FINANCIAL STATEMENTS

31 March 2007

Singapore Airlines 135 Annual Report 2006-07

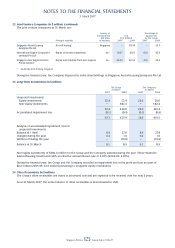

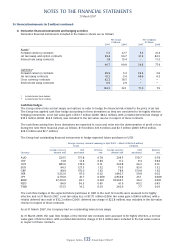

36 Financial Instruments (in $ million) (continued)

(c) Derivative fi nancial instruments and hedging activities

Derivative fi nancial instruments included in the balance sheets are as follows:

The Group The Company

31 March 31 March

2007 2006 2007 2006

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Assets *

Forward currency contracts 5.5 27.7 3.3 21.4

Jet fuel swap and option contracts 39.4 56.7 31.5 44.5

Interest rate swap contracts 1.8 15.4 – 11.5

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

46.7 99.8 34.8 77.4

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Liabilities #

Forward currency contracts 29.9 5.3 22.4 3.6

Jet fuel swap contracts 61.2 5.4 48.6 4.3

Cross currency contracts 42.2 18.5 – –

Interest rate swap contracts 0.9 2.9 – –

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

134.2 32.1 71.0 7.9

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

* Included under trade debtors

# Included under trade creditors

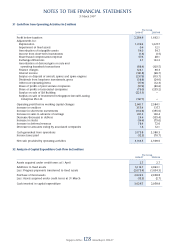

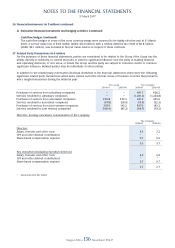

Cash fl ow hedges

The Group entered into jet fuel swaps and options in order to hedge the fi nancial risk related to the price of jet fuel.

The Group has applied cash fl ow hedge accounting to these derivatives as they are considered to be highly effective

hedging instruments. A net fair value gain of $33.7 million (2006: $82.2 million), with a related deferred tax charge of

$18.3 million (2006: $34.5 million), was included in the fair value reserve in respect of these contracts.

The cash fl ows arising from these derivatives are expected to occur and enter into the determination of profi t or loss

during the next three fi nancial years as follows: $17.4 million, $13.6 million and $2.7 million (2006: $55.0 million,

$24.5 million and $2.7 million).

The Group had outstanding fi nancial instruments to hedge expected future purchases in USD:

Foreign currency contracts maturing in April 2007 – March 2008 (in $ million)

Group Company

–––––––––––––––––––––––––––––––––––––––––––––––––––––––– –––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Foreign currency USD Effective Foreign currency USD Effective

Currency amount sold purchased rate amount sold purchased rate

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

AUD 226.5 175.8 0.78 204.5 158.7 0.78

CHF 14.8 12.4 0.84 11.2 9.4 0.84

CNY 885.0 118.0 0.13 346.8 46.2 0.13

EUR 96.3 127.3 1.32 70.3 93.0 1.32

GBP 88.4 170.0 1.92 78.4 150.8 1.92

INR 3,102.0 67.0 0.02 1,842.7 39.8 0.02

JPY 4,710.0 41.7 0.009 2,836.8 25.1 0.009

KRW 27,210.0 29.1 0.001 18,905.7 20.2 0.001

NZD 86.9 56.3 0.65 61.9 40.2 0.65

TWD 513.3 16.2 0.03 242.6 7.7 0.03

The cash fl ow hedges of the expected future purchases in USD in the next 12 months were assessed to be highly

effective and at 31 March 2007, a net fair value loss of $117.1 million (2006: fair value gain of $60.6 million), with a

related deferred tax credit of $32.2 million (2006: deferred tax charge of $22.8 million), was included in the fair value

reserve in respect of these contracts.

As at 31 March 2007, the Company had no outstanding interest rate swaps.

At 31 March 2006, the cash fl ow hedges of the interest rate contracts were assessed to be highly effective, a net fair

value gain of $12.0 million, with a related deferred tax charge of $2.3 million were included in the fair value reserve

in respect of these contracts.