Singapore Airlines 2007 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2007 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

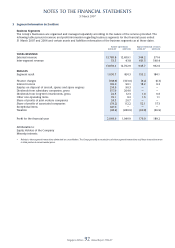

Singapore Airlines 82 Annual Report 2006-07

2 Accounting Policies (continued)

(e) Intangible assets

(i) Goodwill

Goodwill acquired in a business combination is initially measured at cost being the excess of the cost of the

business combination over the Group’s interest in the net fair value of the identifi able assets, liabilities and

contingent liabilities. Following initial recognition, goodwill is measured at cost less any accumulated impairment

losses. Goodwill is reviewed for impairment, annually or more frequently if events or changes in circumstances

indicate that the carrying value may be impaired.

For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date,

allocated to each of the Group’s cash-generating units, or groups of cash-generating units, that are expected to

benefi t from the synergies of the combination, irrespective of whether other assets or liabilities of the Group are

assigned to those units or groups of units. Each unit or group of units to which the goodwill is so allocated:

• represents the lowest level within the Group at which the goodwill is monitored for internal management

purposes; and

• is not larger than a segment based on either the Group’s business or the Group’s geographical reporting

format.

When determining goodwill, assets and liabilities of the acquired interest are translated using the exchange rate

at the date of acquisition if the fi nancial statements of the acquired interest are not denominated in SGD.

A cash-generating unit (or group of cash-generating units) to which goodwill has been allocated are tested

for impairment annually and whenever there is an indication that the unit may be impaired, by comparing

the carrying amount of the unit, including the goodwill, with the recoverable amount of the unit. Where the

recoverable amount of the cash-generating unit (or group of cash-generating units) is less than the carrying

amount, an impairment loss is recognised.

Where goodwill forms part of a cash-generating unit (or group of cash-generating units) and part of the operation

within that unit is disposed of, the goodwill associated with the operation disposed of is included in the carrying

amount of the operation when determining the gain or loss on disposal of the operation. Goodwill disposed of

in this circumstance is measured based on the relative values of the operation disposed of and the portion of the

cash-generating unit retained.

(ii) Computer software

Computer software is stated at cost less accumulated amortisation and accumulated impairment losses, if any.

These costs are amortised using the straight-line method over their estimated useful lives of 1 to 5 years.

(f) Foreign currencies

The management has determined the currency of the primary economic environment in which the Company

operates i.e. functional currency, to be SGD. Sales prices and major costs of providing goods and services including

major operating expenses are primarily infl uenced by fl uctuations in SGD.

Foreign currency transactions are converted into SGD at exchange rates which approximate bank rates prevailing

at dates of transactions, after taking into account the effect of forward currency contracts which expired during the

fi nancial year.

All foreign currency monetary assets and liabilities are translated into SGD using year-end exchange rates.

Non-monetary assets and liabilities are translated using exchange rates that existed when the values were

determined.

Gains and losses arising from conversion of monetary assets and liabilities are taken to the profi t and loss account.

For the purposes of the Group fi nancial statements, the net assets of the foreign subsidiary, associated and joint

venture companies are translated into SGD at the exchange rates ruling at the balance sheet date. The fi nancial

results of foreign subsidiary, associated and joint venture companies are translated monthly into SGD at the

prevailing exchange rates. The resulting gains or losses on exchange are taken to foreign currency translation

reserve.

NOTES TO THE FINANCIAL STATEMENTS

31 March 2007