Western Union 2006 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2006 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Notes to Consolidated Financial Statements 83

The aggregate amount charged to expense in

connection with all of the above plans was $9.2 million,

$8.1 million, and $7.5 million during the years ended

December 31, 2006, 2005, and 2004, respectively.

Defined Benefit Plans

FFMC’s acquisition of WUFSI in November 1994 included

the assumption of $304.0 million of underfunded pension

obligations related to two frozen defined benefit pension

plans. Benefit accruals under these plans were frozen in

1988. First Data reduced these underfunded obligations

by contributing $35.6 million in 2004 to the plans. No

contributions were made by First Data or Western Union

in 2005 and 2006. As part of the Distribution, Western

Union is responsible for any remaining underfunded

pension obligations. Western Union does not currently

anticipate contributing to the plans in 2007. A September 30

measurement date is used for the Company’s plans.

On December 31, 2006, the Company adopted the

recognition and disclosure provisions of SFAS No. 158,

which requires the Company to recognize the funded status

of its pension plans in its Consolidated Balance Sheets as

of December 31, 2006 with a corresponding adjustment

to “Accumulated other comprehensive loss”, net of tax.

Due to the frozen status of the Company’s pension plans,

the Company’s funded status of its pension plans was

already reflected in its Consolidated Balance Sheets, and

therefore, no such adjustment was required to “Pension

obligations”, “Deferred tax liability, net” or “Accumulated

other comprehensive loss” on adoption of SFAS No. 158.

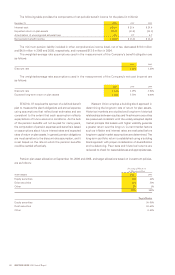

The following table provides a reconciliation of the changes in the pension plans’ benefit obligations and fair value

of assets for the plan years ended September 30, 2006 and 2005, and a statement of the funded status of the plans as

of September 30, 2006 and 2005 (in millions):

September 30, 2006 2005

CHANGE IN BENEFIT OBLIGATION

Projected benefit obligation at October 1, $494.1 $515.7

Interest costs 24.8 25.6

Actuarial (gain)/loss (13.5) 0.4

Benefits paid (46.4) (47.6)

Projected benefit obligation at September 30, 459.0 494.1

CHANGE IN PLAN ASSETS

Fair value of plan assets at October 1, 424.3 432.8

Actual return on plan assets 28.2 39.1

Benefits paid (46.4) (47.6)

Fair value of plan assets at September 30, 406.1 424.3

Funded status of the plan (52.9) (69.8)

Unrecognized amounts, principally unrecognized actuarial loss 98.1 114.2

Total recognized $ 45.2 $ 44.4

Accumulated benefit obligation 459.0 494.1

The pension obligations and changes in the value of

plan assets to meet those obligations are not recognized

as actuarial gains and losses of the plan as they occur but

are recognized systematically over subsequent periods.

These differences are treated as an unrecognized

net gain/loss and not an immediate recognized amount.

Included in “Accumulated other comprehensive loss” at

December 31, 2006 is $3.6 million ($2.3 million net of tax)

of unrecognized actuarial losses that are expected to be

recognized in net periodic pension cost during the year

ended December 31, 2007. No plan assets are expected

to be returned to the Company during the year ended

December 31, 2007.

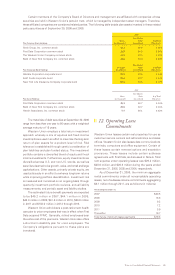

The following table provides the amounts recognized in the Consolidated Balance Sheets (in millions):

December 31, 2006 2005

Accrued benefit liability $(52.9) $(69.8)

Accumulated other comprehensive income 98.1 114.2

Net amount recognized $ 45.2 $ 44.4

For the plan years ended September 30, 2006 and 2005, the projected benefit obligation was equal to the accumulated

benefit obligation.