Western Union 2006 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2006 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

WESTERN UNION 2006 Annual Report 40

||

Revenue is also impacted by prices charged to the

consumer, the amount of money sent, and by changes

in the exchange rate between foreign currencies,

particularly the euro, and the United States

dollar. We have made periodic pricing decreases in

response to competition and to implement our brand

investment strategy, which includes better meeting

consumer needs, maximizing market opportunities

and strengthening our overall competitive positioning.

Pricing decreases generally reduce margins, but are

done in anticipation that they will result in increased

transaction volumes. Such pricing decreases have

averaged approximately 3% of our annual revenues

over the last three years, a trend that is expected

to continue.

|| We continue to face robust competition in both our

consumer-to-consumer and consumer-to-business

segments from a variety of money transfer and

consumer payment providers. We believe the most

significant competitive factors in the consumer-to-

consumer segment relate to brand recognition,

distribution network, consumer experience and price

and in the consumer-to-business segment relate to

brand recognition, convenience, variety of payment

methods and price.

|| Regulation of the money transfer industry is

increasing. The number and complexity of regulations

around the world and the pace at which regulation is

changing are factors that pose significant challenges

to our business. We continue to implement policies

and programs and adapt our business practices and

strategies to help us comply with current legal

requirements, as well as with new and changing

legal requirements affecting particular services, or

the conduct of our business in general. Our activities

include dedicated compliance personnel, training

and monitoring programs, government relations and

regulatory outreach efforts and support and guidance

to the agent network on compliance programs.

These efforts increase our costs of doing business.

||

Our consumer-to-business segment continues to

experience a shift in demand in the United States

from cash-based walk-in payment services to

lower margin, higher volume growth electronic

payment services.

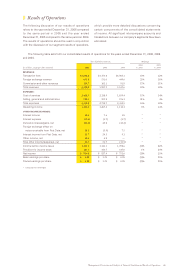

Significant Financial and Other Highlights

Our spin-off from First Data was completed on

September 29, 2006. As such, profit and cash flow

comparisons with prior year are and will continue to

be meaningfully impacted by the fact that, up until

September 29, 2006, we were a segment of First

Data, while now we are a stand alone company. In

particular, interest expense and corporate overhead

costs will be higher in the future than they were in the

past. Significant financial and other highlights for the

year ended December 31, 2006 include:

||

We generated $4,470.2 million in total consolidated

revenues and $1,311.4 million in consolidated

operating income, resulting in year-over-year growth

of 12% and 3% in total consolidated revenues and

operating income, respectively.

|| Consolidated net income during 2006 was

$914.0 million, representing a decrease of 1% from

2005. Basic and diluted earnings per share during

2006 were $1.20 and $1.19, respectively, compared

to basic and diluted earnings per share of $1.21

in 2005.

|| We completed 147 million consumer-to-consumer

transactions worldwide, an increase of 24% over

2005. Excluding transactions attributable to Vigo

Remittance Corporation, or “Vigo,” which was acquired

in October 2005, consumer-to-consumer transactions

increased 17% in 2006 compared to 2005.

||

We completed 249 million consumer-to-business

transactions, an increase of 16% over 2005. Excluding

transactions attributable to SEPSA, consumer-

to-business transactions increased 11% in 2006

compared to 2005.

||

Consolidated cash flow provided by operating activities

was $1,108.9 million, representing an increase of

11% from 2005 consolidated cash flows provided

by operating activities of $1,002.8 million.

The Separation of Western Union from First Data

The spin-off by First Data of its money transfer and

consumer payments business to our company became

effective on September 29, 2006 through a distribution

of 100% of the common stock of The Western Union

Company to the holders of record of First Data’s common

stock (the “Distribution”). The Distribution was pursuant

to the separation and distribution agreement by which First

Data contributed to The Western Union Company the

subsidiaries that operated its money transfer and consumer

payments businesses and its interest in a Western Union

money transfer agent, as well as related assets, including

real estate. First Data received a private letter ruling from

the Internal Revenue Service and an opinion from tax

counsel to the effect that the spin-off was tax free to the

stockholders, First Data and Western Union. First Data

distributed all of the shares of Western Union common

stock as a dividend on First Data common stock as of the

record date for the Distribution.