Volvo 2002 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2002 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

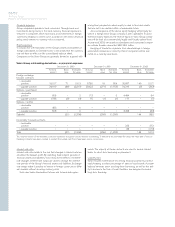

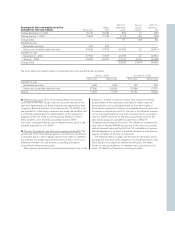

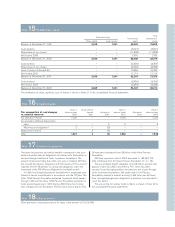

An increase of one percentage point per year in healthcare costs

would change the accumulated post-retirement benefit obligation as

of December 31, 2002 by approximately 191, and the net post-

retirement benefit expense by approximately 14. A decrease of 1%

would decrease the accumulated value of obligations by about 180

and reduce costs by approximately 13. In 2001, an increase of 1%

would increase the accumulated value of obligations by about 206

and increase costs by about 15; a decrease of 1% would reduce the

accumulated value of obligations by about 194 and cut costs by

about 14.

Calculations made as of December 31, 2002 show an annual

increase of 10% in the weighted average per capita costs of cover-

ed health-care benefits; it is assumed that the percentage will

decline gradually to 5% and then remain at that level.

The discount rates used in determining the accumulated post-

retirement benefit obligation as of December 31, 2000, 2001 and

2002 were 7.5%, 7.0-7.25% and 6.75%, respectively.

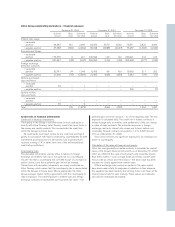

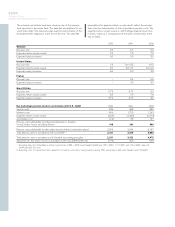

I. Alecta surplus funds. In the mid-1990s and later years surpluses

arose in the Alecta insurance company (previously SPP) since the

return on the management of ITP pension plan exceeded the growth

in pension obligations. As a result of decisions in December 1998,

Alecta distributed, company by company, the surpluses that had

arisen up to and including 1998. In accordance with a statement

issued by a special committee of the Swedish Financial Accounting

Standards Council, surplus funds that were accumulated in Alecta

should be reported in companies when their present value can be

calculated in a reliable manner. The rules governing how the refund

was to be made were established in the spring of 2000 and an

income amounting to 683 was included in the Group’s income state-

ment under Swedish GAAP during 2000. In accordance with U.S

GAAP, the surplus funds should be recognized in the income state-

ment when they are settled.

J. Software development. In accordance with U.S. GAAP (SOP 98–1

“Accounting for the Costs of Computer Software Developed or

Obtained for Internal Use”) expenditures for software development

should be capitalized and amortized over the useful lives of the pro-

jects. In Volvo’s accounting in accordance with U.S. GAAP, SOP 98–1

is applied as of January 1999. In Volvo’s accounts prepared under

Swedish GAAP up to and including 2000, expenditures for software

development were expensed as incurred. Effective in 2001, Volvo

adopted a new Swedish accounting standard, RR15 Intangible

assets. With regard to software development, the new standard is

substantially equivalent to U.S. GAAP and consequently the differ-

ence between Swedish and U.S. GAAP is pertaining only to expen-

ditures for software development during 1999 and 2000.

K. Product development. Effective in 2001, Volvo adopted a new

Swedish accounting standard, RR15 Intangible assets. In accordance

with the new standard, which conforms in all significant respects to

the corresponding standard issued by the International Accounting

Standards Committee (IASC), expenditures for development of new

and existing products should be recognized as intangible assets if

such expenditures with a high degree of certainty will result in future

financial benefits for the company. The acquisition value of such

intangible assets should be amortized over the useful lives of the

assets. In accordance with the new standard, no retroactive applica-

tion is allowed. Under U.S. GAAP, all expenditures for development of

new and existing products should be expensed as incurred.

L. Entrance fees, aircraft engine programs. In connection with its

participation in aircraft engine programs, Volvo Aero in certain cases

pays an entrance fee. In Volvo’s accounting these entrance fees are

capitalized and amortized over 5 to 10 years. In accordance with U.S.

GAAP, these entrance fees are expensed as incurred.

M. Tax effects of U.S. GAAP adjustments. Deferred taxes are

generally reported for temporary differences arising from differences

between U.S. GAAP and Swedish accounting principles. During

2002, a new tax legislation was enacted in Sweden which removed

the possibility to offset capital losses on investments in shares held

for operating purposes against income from operations. As a result

of the new legislation, a tax expense of 2,123 was charged to Volvo’s

net income under U.S. GAAP to reduce the carrying value of deferred

tax assets relating to investments in shares classified as “available-for-

sale".

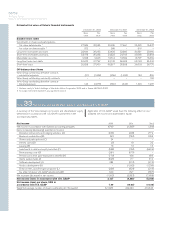

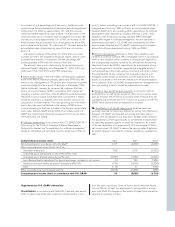

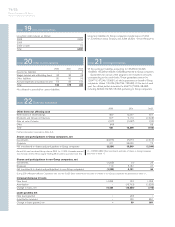

Comprehensive income (loss) 2000 2001 2002

Net income (loss) in accordance with U.S. GAAP 3,127 (4,320) (6,265)

Other comprehensive income (loss), net of tax

Translation differences 966 1,015 (2,222)

Unrealized gains and (losses) on securities (SFAS 115):

Unrealized gains (losses) arising during the year (3,787) (1,532) (2,425)

Less: Reclassification adjustment for (gains) and losses included in net income (1) 733 7,558

Additional minimum liability for pension obligations (FAS 87) (132) (1,622) (3,234)

Other (119) 41 (165)

Other comprehensive income (loss), subtotal (3,073) (1,365) (488)

Comprehensive income (loss) in accordance with U.S. GAAP 54 (5,685) (6,753)

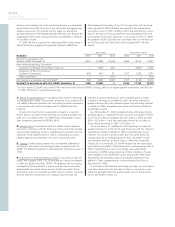

Supplementary U.S. GAAP information

Classification. In accordance with SFAS 95, “cash and cash equiva-

lents” comprise only funds with a maturity of three months or less

from the date of purchase. Some of Volvo’s liquid funds (see Notes

19 and 20) do not meet this requirement. Consequently, in accord-

ance with SFAS 95, changes in this portion of liquid funds should be

reported as investing activities.