Volvo 2002 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2002 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

14/15

Business Areas

Buses

Volvo Buses’ product line comprises

complete buses, bus chassis and bodies

for various applications such as city, inter-

city buses and coaches as well as related

services.

Volvo Buses has renewed its entire

product range in less than five years.

Most of the new models are based on TX,

the company’s product platform for inter-

city buses and tourist coaches. The intro-

duction of platform TX is the largest

industrial project ever within Volvo Buses.

Together with the renowned low floor

chassis B 7 L and the all-round B 7 R

chassis it forms the base for Volvo Buses’

complete bus program.

Volvo Buses has also extended its

range of facilities within servicing and

financing, so as to be able to offer all-

encompassing customer-tailored trans-

port solutions with the best total econ-

omy. This makes it possible for the ope-

rator to predict future costs in the greatest

detail.

Volvo Buses, in cooperation with Volvo

Mobility Systems, offers customized intel-

ligent transport systems. This encom-

passes full control of the buses in opera-

tion, priority traffic light systems as well as

driver information. Travel information for

the passengers as well as vehicle man-

agement and revenue management sys-

tems are also offered.

Tot a l market

The overall market for heavy buses

declined during 2002. The important

European market for Volvo Buses

declined by more than 15% during 2002.

Declines were posted in Germany,

France and Spain. United Kingdom

remained low, while the Nordic region

showed a positive trend. The coach mar-

ket in North America deteriorated further.

The South American market remained

weak. Asia posted some growth.

Business environment

Within OECD, deregulation and privatiza-

tion have altered the operating conditions

for many operators. New actors are pene-

trating and conquering previously restrict-

ed areas, and competition between com-

panies is increasing. There is a move

towards fewer and larger operators who

impose high demands on good economic

overview and better potential for focusing

on their core operations. Important bus

markets in Europe are in a state of reces-

sion which results in increased competition

on other markets.

In North America, the important coach

market is still on a very low level, although

offset by a favorable situation in Mexico.

Important areas like Far East and China

report a considerable growth. In terms of

competitors, a further trend towards con-

solidation among the bus industry is pre-

vailing.

Market share development

Volvo delivered 9,059 (9,953) buses and

bus chassis during 2002. The decline

was mainly attributable to significantly

lower volumes in Mexico and North

America, which were offset to some

extent by favorable volumes in China and

the Nordic countries.

Volvo increased its market shares in

Europe as a result of the prevailing weak

overall market situation in Continental

Europe, where Volvo has relatively low

penetration, and the favorable situation in

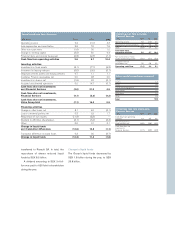

98 99 00 01 02

14 .3 14 .7 17.2 16.7 14.0

Net sales, SEK bn

98 99 00 01 02

385 224 440 (524) (94)

Operating income*, SEK M

98 99 00 01 02

2.71.5 2.6 (3.1) (0.7)

Operating Margin*, %

Net sales as percentage of Volvo Group sales, %

0

0

*excluding restructuring costs

*excluding restructuring costs

8%