Volvo 2002 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2002 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

56/57

The Volvo Group

Notes to consolidated financial statements

Interest-rate risks

Interest-rate risks relate to the risk that changes in interest-rate lev-

els affect the Group’s profit. By matching fixed-interest periods of

financial assets and liabilities, Volvo reduces the effects of interest-

rate changes. Interest-rate swaps are used to change the interest-

rate periods of the Group’s financial assets and liabilities. Exchange-

rate swaps make it possible to borrow in foreign currencies in differ-

ent markets without incurring currency risks.

Volvo also holds standardized futures and forward-rate agree-

ments. The majority of these contracts are used to secure interest

levels for short-term borrowing or placement.

Liquidity risks

Volvo ensures maintenance of a strong financial position by continu-

ously keeping a certain percentage of sales in liquid assets. A proper

balance between short- and long-term borrowing, as well as the abil-

ity to borrow in the form of credit facilities, are designed to ensure

long-term financing.

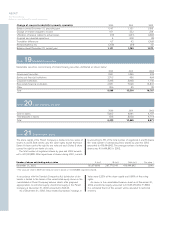

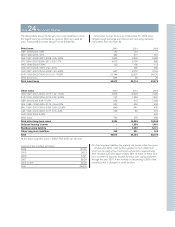

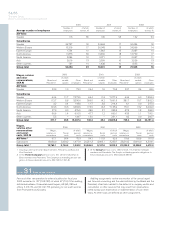

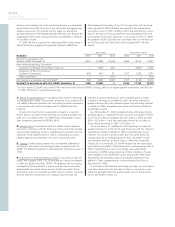

Volvo Group outstanding derivatives – commercial exposure

December 31, 2000 December 31, 2001 December 31, 2002

Notional Book Estimated Notional Book Estimated Notional Book Estimated

amount value fair value amount value fair value amount value fair value

Foreign exchange

forward contracts

– receivable

position 19,017 71 1,513 9,780 16 554 25,857 149 1,017

– payable position 24,910 (89) (2,817) 20,022 (271) (1,753) 10,210 (5) (202)

Options – purchased

– receivable

position 808 – 2 173 – 0 4,484 – 94

– payable position 1,736 (3) (4) 75 (1) (1) 117 – (1)

Options – written

– receivable

position 385 – 0––––––

– payable position 568 – 0–––3,458 – (53)

Subtotal (21) (1,306) (256) (1,200) 144 855

Commodity forward contracts

– receivable

position ––––––223–272

– payable position ––––––88–(113)

Total (21) (1,306) (256) (1,200) 144 1,014

The notional amount of the derivative contracts represents the gross contract amount outstanding. To determine the estimated fair value, the major part of the out-

standing contracts have been marked to market. Discounted cash flows have been used in some cases.

Financial exposure

Group companies operate in local currencies. Through loans and

investments being mainly in the local currency, financial exposure is

reduced. In companies which have loans and investments in foreign

currencies, hedging is carried out in accordance with Volvo’s financial

policy, which means no currency risks is assumed.

Equity exposure

In conjunction with translation of the Group’s assets and liabilities in

foreign subsidiaries to Swedish kronor a risk arises that the currency

rate will have an effect on the consolidated balance sheet.

Companies in the Volvo Group are generally formed or acquired with

a long-term perspective, where equity is used to fund real assets

that are not to be realized within a foreseeable future.

As a consequence of the above, equity hedging will primarily be

used if a foreign Volvo Group company is over capitalized. To avoid

extensive equity exposure, the level of equity in Volvo Group compa-

nies will be kept at a commercially, legally and fiscally optimal level.

At year-end 2002, net assets in subsidiaries and associated compan-

ies outside Sweden amounted SEK 23.8 billion.

Hedging of translation exposure from shareholdings in foreign

associated companies or minority interest companies will be exe-

cuted on a case-by-case basis.