Volvo 2002 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2002 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

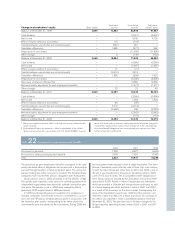

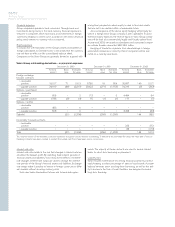

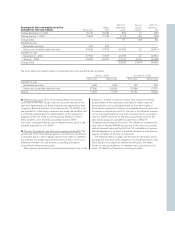

Volvo Group outstanding derivatives – financial exposure

December 31, 2000 December 31, 2001 December 31, 2002

Notional Book Estimated Notional Book Estimated Notional Book Estimated

amount value fair value amount value fair value amount value fair value

Interest-rate swaps

– receivable

position 64,345 561 2,990 62,456 3,670 4,549 78,571 2,822 4,404

– payable position 57,488 (366) (2,969) 86,328 (3,888) (4,633) 73,257 (1,568) (2,536)

Forwards and futures

– receivable

position 174,576 0 201 230,323 120 120 260,921 216 216

– payable position 201,657 (28) (247) 250,390 (126) (126) 255,503 (217) (220)

Foreign exchange

derivative contracts

– receivable

position 32,741 34 1,046 6,306 96 100 15,962 211 202

– payable position 21,668 (76) (2,894) 21,465 (428) (435) 5,443 (70) (72)

Options purchased,

caps and floors

– receivable

position 52 – 1––––––

– payable position ––––––200–(7)

Options written,

caps and floors

– receivable

position –––––––––

– payable position 55 – 0––––––

Total 125 (1,873) (556) (425) 1,394 1,987

Credit risks in financial instruments

Credit risk in financial investments

The liquidity in the Group is invested mainly in local cash pools or

directly with Volvo Treasury. Volvo Treasury invests the liquid funds in

the money and capital markets. This concentrates the credit risk

within the Group’s in-house bank.

All investments must meet criteria for low credit risk and high li-

quidity. In accordance with Volvo’s credit policy, counterparties for both

investments and transactions in derivatives must in general have

received a rating of “A” or better from one of the well-established

credit-rating institutions.

Counterparty risks

The derivative instruments used by Volvo to reduce its foreign-

exchange and interest-rate risk in turn give rise to a counterparty

risk, the risk that a counterparty will not fulfill its part of a forward or

option contract, and that a potential gain will not be realized.

Transactions with derivative instruments are mainly conducted via

Volvo Treasury which means that the counterparty risk is concentrated

within the Group’s in-house bank. Where appropriate, the Volvo

Group arranges master netting agreements with the counterparty to

reduce exposure. The credit exposure in interest-rate and foreign

exchange contracts is represented by the positive fair value – the

potential gain on these contracts – as of the reporting date. The risk

exposure is calculated daily. The credit risk in futures contracts is

limited through daily or monthly cash settlements of the net change

in value of open contracts. The estimated exposure in foreign

exchange contracts, interest-rate swaps and futures, options and

commodity forward contracts amounted to 1,219; 4,620; 94 and

272 as of December 31, 2002.

Volvo does not have any significant exposure to an individual cus-

tomer or counterparty.

Calculation of fair value of financial instruments

Volvo has used generally accepted methods to calculate the market

value of the Group’s financial instruments as of December 31, 2000,

2001 and 2002. In the case of instruments with maturities shorter

than three months – such as liquid funds and certain current liabil-

ities as well as certain short-term loans – the book value has been

assumed to closely approximate market value.

Official exchange rates and prices quoted in the open market

have been used initially for purposes of valuation. In their absence,

the valuation has been made by discounting future cash flows at the

market interest rate for each maturity. These values are estimates

and will not necessarily be realized.