UPS 2015 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2015 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

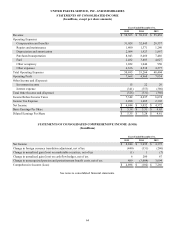

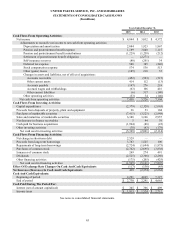

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

59

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

We are exposed to market risk from changes in certain commodity prices, foreign currency exchange rates, interest rates

and equity prices. All of these market risks arise in the normal course of business, as we do not engage in speculative trading

activities. In order to manage the risk arising from these exposures, we utilize a variety of commodity, foreign exchange and

interest rate forward contracts, options and swaps. A discussion of our accounting policies for derivative instruments and

further disclosures are provided in note 15 to the consolidated financial statements.

Commodity Price Risk

We are exposed to changes in the prices of refined fuels, principally jet-A, diesel and unleaded gasoline, as well as

changes in the price of natural gas. Currently, the fuel surcharges that we apply to our domestic and international package and

LTL services are the primary means of reducing the risk of adverse fuel price changes. Additionally, we periodically use a

combination of option, forward and futures contracts to provide partial protection from changing fuel and energy prices. As of

December 31, 2015 and 2014, however, we had no commodity contracts outstanding.

Foreign Currency Exchange Risk

We have foreign currency risks related to our revenue, operating expenses and financing transactions in currencies other

than the local currencies in which we operate. We are exposed to currency risk from the potential changes in functional

currency values of our foreign currency-denominated assets, liabilities and cash flows. Our most significant foreign currency

exposures relate to the Euro, British Pound Sterling, Canadian Dollar, Chinese Renminbi and Hong Kong Dollar. We use

forwards as well as a combination of purchased and written options to hedge forecasted cash flow currency exposures. These

derivative instruments generally cover forecasted foreign currency exposures for periods of 12 to 48 months. We also utilize

forward contracts to hedge portions of our anticipated cash settlements of intercompany transactions subject to foreign currency

remeasurement.

Interest Rate Risk

We have issued debt instruments, including debt associated with capital leases, that accrue expense at fixed and floating

rates of interest. We use a combination of interest rate swaps as part of our program to manage the fixed and floating interest

rate mix of our total debt portfolio and related overall cost of borrowing. The notional amount, interest payment and maturity

dates of the swaps match the terms of the associated debt. We also utilize forward starting swaps and similar instruments to

lock in all or a portion of the borrowing cost of anticipated debt issuances. Our floating rate debt and interest rate swaps subject

us to risk resulting from changes in short-term (primarily LIBOR) interest rates.

We also are subject to interest rate risk with respect to our pension and postretirement benefit obligations, as changes in

interest rates will effectively increase or decrease our liabilities associated with these benefit plans, which also results in

changes to the amount of pension and postretirement benefit expense recognized in future periods.

We have investments in debt securities, as well as cash-equivalent instruments, some of which accrue income at variable

rates of interest. Additionally, we hold a portfolio of finance receivables that accrue income at fixed and floating rates of

interest.

Equity Price Risk

We hold investments in various common equity securities that are subject to price risk.

Sensitivity Analysis

The following analysis provides quantitative information regarding our exposure to foreign currency exchange risk,

interest rate risk and equity price risk embedded in our existing financial instruments. We utilize valuation models to evaluate

the sensitivity of the fair value of financial instruments with exposure to market risk that assume instantaneous, parallel shifts

in exchange rates, interest rate yield curves and commodity and equity prices. For options and instruments with non-linear

returns, models appropriate to the instrument are utilized to determine the impact of market shifts.