UPS 2014 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2014 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

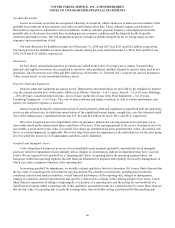

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

56

Pension and Postretirement Medical Benefits

Our pension and other postretirement benefit costs are calculated using various actuarial assumptions and methodologies.

These assumptions include discount rates, health care cost trend rates, inflation, compensation increase rates, expected returns

on plan assets, mortality rates and other factors. The assumptions utilized in recording the obligations under our plans represent

our best estimates, and we believe that they are reasonable, based on information as to historical experience and performance as

well as other factors that might cause future expectations to differ from past trends.

Differences in actual experience or changes in assumptions may affect our pension and other postretirement obligations

and future expense. The primary factors contributing to actuarial gains and losses each year are (1) changes in the discount rate

used to value pension and postretirement benefit obligations as of the measurement date, (2) differences between the expected

and the actual return on plan assets, (3) changes in demographic assumptions including mortality and (4) participant experience

different from demographic assumptions.

We recognize changes in the fair value of plan assets and net actuarial gains or losses in excess of a corridor (defined as

10% of the greater of the fair value of plan assets or the plans' projected benefit obligations) in pension expense annually at

December 31st each year. The remaining components of pension expense (herein referred to as "ongoing net periodic benefit

cost"), primarily service and interest costs and the expected return on plan assets, are recorded on a quarterly basis.

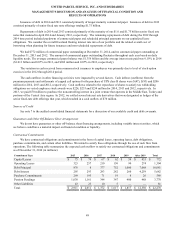

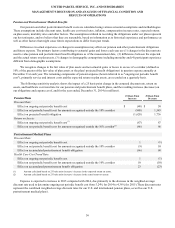

The following sensitivity analysis shows the impact of a 25 basis point change in the assumed discount rate, return on

assets, and healthcare cost trend rate for our pension and postretirement benefit plans, and the resulting increase (decrease) on

our obligations and expense as of, and for the year ended, December 31, 2014 (in millions).

Pension Plans 25 Basis Point

Increase

25 Basis Point

Decrease

Discount Rate:

Effect on ongoing net periodic benefit cost $ (48)$ 50

Effect on net periodic benefit cost for amounts recognized outside the 10% corridor (888) 1,543

Effect on projected benefit obligation (1,628) 1,736

Return on Assets:

Effect on ongoing net periodic benefit cost(1) (67)67

Effect on net periodic benefit cost for amounts recognized outside the 10% corridor(2) (66)66

Postretirement Medical Plans

Discount Rate:

Effect on ongoing net periodic benefit cost 1 (1)

Effect on net periodic benefit cost for amounts recognized outside the 10% corridor (9)10

Effect on accumulated postretirement benefit obligation (66)68

Health Care Cost Trend Rate:

Effect on ongoing net periodic benefit cost 1 (1)

Effect on net periodic benefit cost for amounts recognized outside the 10% corridor 10 (10)

Effect on accumulated postretirement benefit obligation 23 (23)

(1) Amount calculated based on 25 basis point increase / decrease in the expected return on assets.

(2) Amount calculated based on 25 basis point increase / decrease in the actual return on assets.

Expense is expected to increase in 2015 compared with 2014, due primarily to the decrease in the weighted-average

discount rate used to determine ongoing net periodic benefit cost from 5.24% for 2014 to 4.36% for 2015 (These discount rates

represent the combined weighted-average discount rates for our U.S. and international pension plans, as well as our U.S.

postretirement medical plans).