UPS 2013 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2013 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

47

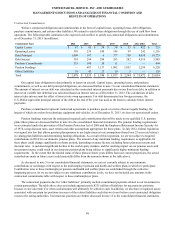

Cash received from common stock issuances to employees increased primarily due to additional stock option exercises in

2013 and 2012.

The cash outflows in other financing activities were impacted by several factors. Cash inflows (outflows) from the

premium payments and settlements of capped call options for the purchase of UPS class B shares were $(93), $206 and $(200)

million for 2013, 2012 and 2011, respectively. In 2013, we paid $70 million to purchase the noncontrolling interest in a joint

venture that operates in the Middle East, Turkey and portions of the Central Asia region. In 2012, we settled several interest

rate derivatives that were designated as hedges of the senior fixed-rate debt offerings that year, which resulted in a cash outflow

of $70 million. The remaining cash outflows in other financing activities for 2013, 2012 and 2011 were related to the

repurchase of shares to satisfy tax withholding obligations on vested employee stock awards.

Sources of Credit

We are authorized to borrow up to $10.0 billion under our U.S. commercial paper program. We also maintain a European

commercial paper program under which we are authorized to borrow up to €5.0 billion in a variety of currencies. No amounts

were outstanding under these programs as of December 31, 2013. The amount of commercial paper outstanding under these

programs in 2014 is expected to fluctuate.

We maintain two credit agreements with a consortium of banks. One of these agreements provides revolving credit

facilities of $1.5 billion, and expires on March 28, 2014. Generally, amounts outstanding under this facility bear interest at a

periodic fixed rate equal to LIBOR for the applicable interest period and currency denomination, plus an applicable margin.

Alternatively, a fluctuating rate of interest equal to the highest of (1) JPMorgan Chase Bank’s publicly announced prime rate,

(2) the Federal Funds effective rate plus 0.50%, and (3) LIBOR for a one month interest period plus 1.00%, plus an applicable

margin, may be used at our discretion. In each case, the applicable margin for advances bearing interest based on LIBOR is a

percentage determined by quotations from Markit Group Ltd. for our 1-year credit default swap spread, subject to a minimum

rate of 0.10% and a maximum rate of 0.75%. The applicable margin for advances bearing interest based on the prime rate is

1.00% below the applicable margin for LIBOR advances (but not lower than 0.00%). We are also able to request advances

under this facility based on competitive bids for the applicable interest rate. There were no amounts outstanding under this

facility as of December 31, 2013.

The second agreement provides revolving credit facilities of $1.0 billion, and expires on March 29, 2018. Generally,

amounts outstanding under this facility bear interest at a periodic fixed rate equal to LIBOR for the applicable interest period

and currency denomination, plus an applicable margin. Alternatively, a fluctuating rate of interest equal to the highest of (1)

JPMorgan Chase Bank’s publicly announced prime rate, (2) the Federal Funds effective rate plus 0.50%, and (3) LIBOR for a

one month interest period plus 1.00%, plus an applicable margin, may be used at our discretion. In each case, the applicable

margin for advances bearing interest based on LIBOR is a percentage determined by quotations from Markit Group Ltd. for our

credit default swap spread, interpolated for a period from the date of determination of such credit default swap spread in

connection with a new interest period until the latest maturity date of this facility then in effect (but not less than a period of

one year). The applicable margin is subject to certain minimum rates and maximum rates based on our public debt ratings from

Standard & Poor’s Rating Service and Moody’s Investors Service. The minimum applicable margin rates range from 0.100% to

0.375%, and the maximum applicable margin rates range from 0.750% to 1.250% per annum. The applicable margin for

advances bearing interest based on the prime rate is 1.00% below the applicable margin for LIBOR advances (but not less than

0.00%). We are also able to request advances under this facility based on competitive bids. There were no amounts outstanding

under this facility as of December 31, 2013.

Our existing debt instruments and credit facilities subject us to certain financial covenants. As of December 31, 2013 and

for all prior periods presented, we have satisfied these financial covenants. These covenants limit the amount of secured

indebtedness that we may incur, and limit the amount of attributable debt in sale-leaseback transactions, to 10% of net tangible

assets. As of December 31, 2013, 10% of net tangible assets is equivalent to $2.612 billion; however, we have no covered sale-

leaseback transactions or secured indebtedness outstanding. We do not expect these covenants to have a material impact on our

financial condition or liquidity.

Guarantees and Other Off-Balance Sheet Arrangements

We do not have guarantees or other off-balance sheet financing arrangements, including variable interest entities, which

we believe could have a material impact on financial condition or liquidity.