UPS 2010 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

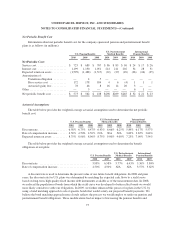

postretirement medical benefits discount rate on average 31 and 51 basis points for 2009 and 25 and 17 basis

points for 2008. For 2010, each basis point increase in the discount rate decreases the projected benefit obligation

by approximately $32 million and $4 million for pension and postretirement medical benefits, respectively. For

our international plans, the discount rate is determined by matching the expected cash flows of a sample plan of

similar duration to a yield curve based on long-term, high quality fixed income debt instruments available as of

the measurement date. These assumptions are updated annually.

An assumption for expected return on plan assets is used to determine a component of net periodic benefit

cost for the fiscal year. This assumption for our U.S. plans was developed using a long-term projection of returns

for each asset class, and taking into consideration our target asset allocation. The expected return for each asset

class is a function of passive, long-term capital market assumptions and excess returns generated from active

management. The capital market assumptions used are provided by independent investment advisors, while

excess return assumptions are supported by historical performance, fund mandates and investment expectations.

In addition, we compare the expected return on asset assumption with the average historical rate of return these

plans have been able to generate.

For the UPS Retirement Plan, we use a market-related valuation method for recognizing investment gains or

losses. Investment gains or losses are the difference between the expected and actual return based on the market-

related value of assets. This method recognizes investment gains or losses over a five year period from the year

in which they occur, which reduces year-to-year volatility in pension expense. Thus, a portion of the investment

losses we incurred during 2008 will be deferred through 2012. Our expense in future periods will be impacted as

gains or losses are recognized in the market-related value of assets.

For plans outside the U.S., consideration is given to local market expectations of long-term returns.

Strategic asset allocations are determined by country, based on the nature of liabilities and considering the

demographic composition of the plan participants.

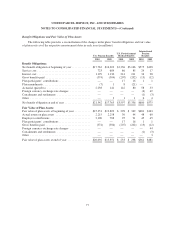

Health care cost trends are used to project future postretirement benefits payable from our plans. For

year-end 2010 U.S. plan obligations, future postretirement medical benefit costs were forecasted assuming an

initial annual increase of 7.5%, decreasing to 5.0% by the year 2017 and with consistent annual increases at those

ultimate levels thereafter.

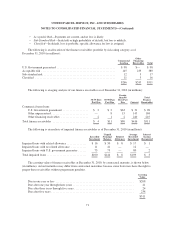

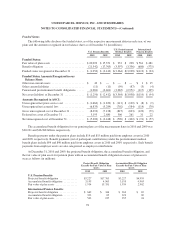

Assumed health care cost trends can have a significant effect on the amounts reported for the U.S.

postretirement medical plans. A one-percent change in assumed health care cost trend rates would have had the

following effects on 2010 results (in millions):

1% Increase 1% Decrease

Effect on total of service cost and interest cost ...................... $ 9 $ (9)

Effect on postretirement benefit obligation ......................... $74 $(78)

76