UPS 2010 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

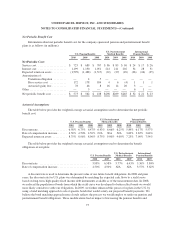

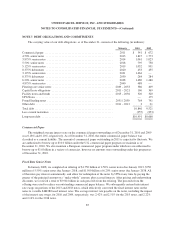

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

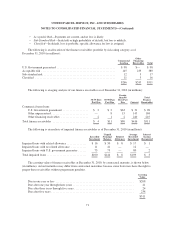

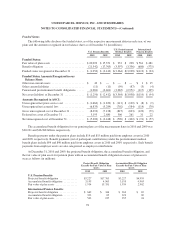

Net Periodic Benefit Cost

Information about net periodic benefit cost for the company-sponsored pension and postretirement benefit

plans is as follows (in millions):

U.S. Pension Benefits

U.S. Postretirement

Medical Benefits

International

Pension Benefits

2010 2009 2008 2010 2009 2008 2010 2009 2008

Net Periodic Cost:

Service cost .................... $ 723 $ 689 $ 707 $ 86 $ 85 $ 96 $ 24 $ 17 $ 26

Interest cost .................... 1,199 1,130 1,051 214 211 202 34 28 31

Expected return on assets .......... (1,599) (1,488) (1,517) (22) (27) (49) (36) (26) (35)

Amortization of:

Transition obligation ......... — 4 5 ——————

Prior service cost ............ 172 178 184 4 6 (4) 1 1 1

Actuarial (gain) loss .......... 78 46 8 16 14 20 3 — —

Other .......................... — 3 ———— 6 1—

Net periodic benefit cost .......... $ 573 $ 562 $ 438 $298 $289 $265 $ 32 $ 21 $ 23

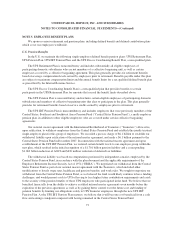

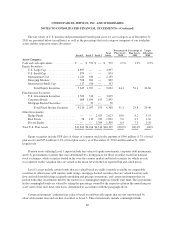

Actuarial Assumptions

The table below provides the weighted-average actuarial assumptions used to determine the net periodic

benefit cost.

U.S. Pension Benefits

U.S. Postretirement

Medical Benefits

International

Pension Benefits

2010 2009 2008 2010 2009 2008 2010 2009 2008

Discount rate .................... 6.58% 6.75% 6.47% 6.43% 6.66% 6.25% 5.84% 6.17% 5.57%

Rate of compensation increase ...... 4.50% 4.50% 4.50% N/A N/A N/A 3.62% 3.65% 3.64%

Expected return on assets .......... 8.75% 8.96% 8.96% 8.75% 9.00% 9.00% 7.25% 7.09% 7.54%

The table below provides the weighted-average actuarial assumptions used to determine the benefit

obligations of our plans.

U.S. Pension Benefits

U.S. Postretirement

Medical Benefits

International

Pension Benefits

2010 2009 2010 2009 2010 2009

Discount rate .................................. 5.98% 6.58% 5.77% 6.43% 5.36% 5.84%

Rate of compensation increase ..................... 4.50% 4.50% N/A N/A 3.57% 3.62%

A discount rate is used to determine the present value of our future benefit obligations. In 2008 and prior

years, the discount rate for U.S. plans was determined by matching the expected cash flows to a yield curve

based on long-term, high quality fixed income debt instruments available as of the measurement date. In 2008,

we reduced the population of bonds from which the yield curve was developed to better reflect bonds we would

more likely consider to settle our obligations. In 2009, we further enhanced this process for plans in the U.S. by

using a bond matching approach to select specific bonds that would satisfy our projected benefit payments. We

believe the bond matching approach more closely reflects the process we would employ to settle our pension and

postretirement benefit obligations. These modifications had an impact of increasing the pension benefits and

75