UPS 2010 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

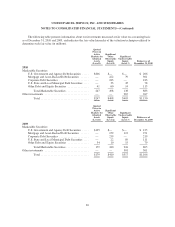

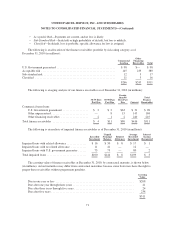

Fair Value Measurements

Our financial assets and liabilities measured at fair value on a recurring basis have been categorized based

upon a fair value hierarchy. Level 1 inputs utilize quoted prices in active markets for identical assets or liabilities.

Level 2 inputs are based on other observable market data, such as quoted prices for similar assets and liabilities,

and inputs other than quoted prices that are observable, such as interest rates and yield curves. Level 3 inputs are

developed from unobservable data reflecting our own assumptions, and include situations where there is little or

no market activity for the asset or liability.

Certain non-financial assets and liabilities are measured at fair value on a nonrecurring basis, including

property, plant, and equipment, goodwill, and intangible assets. These assets are not measured at fair value on a

recurring basis; however, they are subject to fair value adjustments in certain circumstances, such as when there

is evidence of an impairment. A general description of the valuation methodologies used for assets and liabilities

measured at fair value, including the general classification of such assets and liabilities pursuant to the valuation

hierarchy, is included in each footnote with fair value measurements present.

Derivative Instruments

All financial derivative instruments are recorded on our balance sheet at fair value. Derivatives not

designated as hedges must be adjusted to fair value through income. If a derivative is designated as a hedge,

depending on the nature of the hedge, changes in its fair value that are considered to be effective, as defined,

either offset the change in fair value of the hedged assets, liabilities, or firm commitments through income, or are

recorded in AOCI until the hedged item is recorded in income. Any portion of a change in a derivative’s fair

value that is considered to be ineffective, or is excluded from the measurement of effectiveness, is recorded

immediately in income.

Recently Adopted Accounting Standards

Provisions within the following accounting standards were adopted during the years covered by these

consolidated financial statements:

Financial Instruments: The Financial Accounting Standards Board (“FASB”) issued guidance in February

2007 that gives entities the option to measure eligible financial assets, financial liabilities and firm

commitments at fair value (i.e., the fair value option), on an instrument-by-instrument basis, that are

otherwise not accounted for at fair value under other accounting standards. The election to use the fair value

option is available at specified election dates, such as when an entity first recognizes a financial asset or

financial liability or upon entering into a firm commitment. Subsequent changes in fair value must be

recorded in earnings. Additionally, this guidance allowed for a one-time election for existing positions upon

adoption, with the transition adjustment recorded to beginning retained earnings. We adopted this standard

on January 1, 2008, and elected to apply the fair value option to our investment in certain investment

partnerships that were previously accounted for under the equity method. Accordingly, we recorded a $16

62