UPS 2010 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

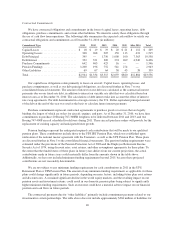

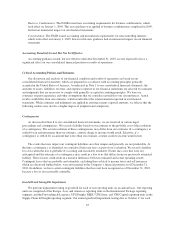

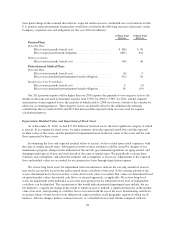

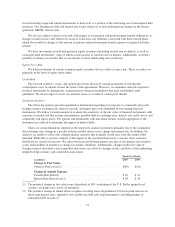

basis point change in the assumed discount rate, expected return on assets, and health care cost trend rate for the

U.S. pension and postretirement benefit plans would have resulted in the following increases (decreases) on the

Company’s reported costs and obligations for the year 2010 (in millions):

25 Basis Point

Increase

25 Basis Point

Decrease

Pension Plans

Discount Rate:

Effect on net periodic benefit cost .......................... $ (86) $ 96

Effect on projected benefit obligation ....................... (805) 854

Return on Assets:

Effect on net periodic benefit cost .......................... (46) 46

Postretirement Medical Plans

Discount Rate:

Effect on net periodic benefit cost .......................... (6) 5

Effect on accumulated postretirement benefit obligation ......... (92) 96

Health Care Cost Trend Rate:

Effect on net periodic benefit cost .......................... 3 (3)

Effect on accumulated postretirement benefit obligation ......... 18 (19)

Our 2011 pension expense will be higher than our 2010 expense due primarily to two negative factors: the

decline in discount rate used to determine expense from 6.58% for 2010 to 5.98% for 2011, and the required

amortization of unrecognized losses, the majority of which relate to 2008 asset losses, outside of the corridor we

utilize for accounting purposes. These negative factors are partially offset by the additional discretionary

contributions that we made in 2010 and 2011 that increased the expected return on assets used for expense

calculation purposes.

Depreciation, Residual Value, and Impairment of Fixed Assets

As of December 31, 2010, we had $17.387 billion of net fixed assets, the most significant category of which

is aircraft. In accounting for fixed assets, we make estimates about the expected useful lives and the expected

residual values of the assets, and the potential for impairment based on the fair values of the assets and the cash

flows generated by these assets.

In estimating the lives and expected residual values of aircraft, we have relied upon actual experience with

the same or similar aircraft types. Subsequent revisions to these estimates could be caused by changes to our

maintenance program, changes in the utilization of the aircraft, governmental regulations on aging aircraft, and

changing market prices of new and used aircraft of the same or similar types. We periodically evaluate these

estimates and assumptions, and adjust the estimates and assumptions as necessary. Adjustments to the expected

lives and residual values are accounted for on a prospective basis through depreciation expense.

We review long-lived assets for impairment when circumstances indicate the carrying amount of an asset

may not be recoverable based on the undiscounted future cash flows of the asset. If the carrying amount of the

asset is determined not to be recoverable, a write-down to fair value is recorded. Fair values are determined based

on quoted market values, discounted cash flows, or external appraisals, as applicable. We review long-lived

assets for impairment at the individual asset or the asset group level for which the lowest level of independent

cash flows can be identified. The circumstances that would indicate potential impairment may include, but are

not limited to, a significant change in the extent to which an asset is utilized, a significant decrease in the market

value of an asset, and operating or cash flow losses associated with the use of the asset. In estimating cash flows,

we project future volume levels for our different air express products in all geographic regions in which we do

business. Adverse changes in these volume forecasts, or a shortfall of our actual volume compared with our

48