UPS 2010 Annual Report Download - page 25

Download and view the complete annual report

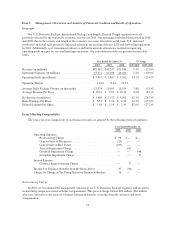

Please find page 25 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

the transportation industry. These requirements may change periodically as a result of regulatory and legislative

requirements and in response to evolving threats. We cannot determine the effect that these new requirements

will have on our cost structure or our operating results, and these rules or other future security requirements may

increase our costs of operations and reduce operating efficiencies. Regardless of our compliance with security

requirements or the steps we take to secure our facilities or fleet, we could be the target of an attack or security

breaches could occur, which could adversely affect our operations or our reputation.

We may be affected by global climate change or by legal, regulatory or market responses to such potential

change.

Concern over climate change, including the impact of global warming, has led to significant federal, state,

and international legislative and regulatory efforts to limit greenhouse gas (“GHG”) emissions. For example, in

the past several years, the U.S. Congress has considered various bills that would regulate GHG emissions. While

these bills have not yet received sufficient Congressional support for enactment, some form of federal climate

change legislation is possible in the future. Even in the absence of such legislation, the Environmental Protection

Agency, spurred by judicial interpretation of the Clean Air Act, may regulate GHG emissions, especially aircraft

or diesel engine emissions, and this could impose substantial costs on us. These costs include an increase in the

cost of the fuel and other energy we purchase and capital costs associated with updating or replacing our aircraft

or trucks prematurely. Until the timing, scope and extent of any future regulation becomes known, we cannot

predict its effect on our cost structure or our operating results. Notwithstanding our widely recognized position as

a leader in sustainable business practices, it is reasonably possible, however, that such legislation or regulation

could impose material costs on us. Moreover, even without such legislation or regulation, increased awareness

and any adverse publicity in the global marketplace about the GHGs emitted by companies in the airline and

transportation industries could harm our reputation and reduce customer demand for our services, especially our

air services.

Strikes, work stoppages and slowdowns by our employees could adversely affect our business, financial

position and results of operations.

A significant number of our employees are employed under a national master agreement and various

supplemental agreements with local unions affiliated with the International Brotherhood of Teamsters and our

airline pilots, airline mechanics, ground mechanics and certain other employees are employed under other

collective bargaining agreements. Strikes, work stoppages and slowdowns by our employees could adversely

affect our ability to meet our customers’ needs, and customers may do more business with competitors if they

believe that such actions or threatened actions may adversely affect our ability to provide services. We may face

permanent loss of customers if we are unable to provide uninterrupted service, and this could adversely affect our

business, financial position and results of operations. The terms of future collective bargaining agreements also

may affect our competitive position and results of operations.

We are exposed to the effects of changing prices of energy, including gasoline, diesel and jet fuel, and

interruptions in supplies of these commodities.

Changing fuel and energy costs may have a significant impact on our operations. We require significant

quantities of fuel for our aircraft and delivery vehicles and are exposed to the risk associated with variations in

the market price for petroleum products, including gasoline, diesel and jet fuel. We mitigate our exposure to

changing fuel prices through our indexed fuel surcharges and we may also enter into hedging transactions from

time to time. If we are unable to maintain or increase our fuel surcharges, higher fuel costs could adversely

impact our operating results. Even if we are able to offset the cost of fuel with our surcharges, high fuel

surcharges may result in a mix shift from our higher yielding air products to lower yielding ground products or

an overall reduction in volume. If fuel prices rise sharply, even if we are successful in increasing our fuel

surcharge, we could experience a lag time in implementing the surcharge, which could adversely affect our short-

term operating results. There can be no assurance that our hedging transactions will be effective to protect us

13