UPS 2010 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2010 UPS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

UNITED PARCEL SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

We have designated and account for interest rate swaps that convert fixed rate interest payments into

floating rate interest payments as hedges of the fair value of the associated debt instruments. Therefore, the gains

and losses resulting from fair value adjustments to the interest rate swaps and fair value adjustments to the

associated debt instruments are recorded to interest expense in the period in which the gains and losses occur. We

have designated and account for interest rate swaps that convert floating rate interest payments into fixed rate

interest payments as cash flow hedges of the forecasted payment obligations. The gains and losses resulting from

fair value adjustments to the interest rate swap are recorded to AOCI.

We periodically hedge the forecasted fixed-coupon interest payments associated with anticipated debt

offerings, using forward starting interest rate swaps, interest rate locks, or similar derivatives. These agreements

effectively lock a portion of our interest rate exposure between the time the agreement is entered into and the

date when the debt offering is completed, thereby mitigating the impact of interest rate changes on future interest

expense. These derivatives are settled commensurate with the issuance of the debt, and any gain or loss upon

settlement is amortized as an adjustment to the effective interest yield on the debt.

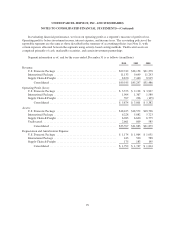

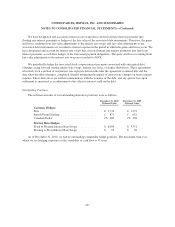

Outstanding Positions

The notional amounts of our outstanding derivative positions were as follows:

December 31, 2010

Notional Value

December 31, 2009

Notional Value

Currency Hedges:

Euro ....................................... €1,732 €1,372

British Pound Sterling ......................... £ 871 £ 692

Canadian Dollar .............................. C$ 289 C$ 228

Interest Rate Hedges:

Fixed to Floating Interest Rate Swaps ............. $ 6,000 $ 3,751

Floating to Fixed Interest Rate Swaps ............. $ 53 $ 28

As of December 31, 2010, we had no outstanding commodity hedge positions. The maximum term over

which we are hedging exposures to the variability of cash flow is 39 years.

107