U-Haul 2016 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2016 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

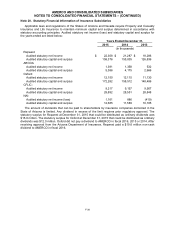

AMERCO AND CONSOLIDATED SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – (CONTINUED)

F-28

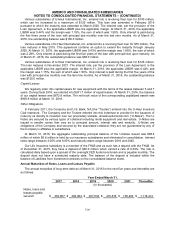

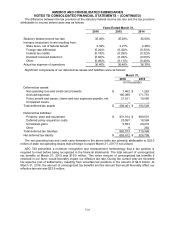

Future net benefit payments are expected as follows:

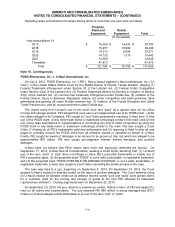

Future Net Benefit

Payments

(In thousands)

Year-ended:

2017

$

658

2018

773

2019

914

2020

1,073

2021

1,263

2022 through 2026

9,169

Total

$

13,850

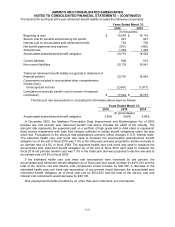

Note 15. Fair Value Measurements

Fair values of cash equivalents approximate carrying value due to the short period of time to maturity.

Fair values of short term investments, investments available-for-sale, long term investments, mortgage

loans and notes on real estate, and interest rate swap contracts are based on quoted market prices,

dealer quotes or discounted cash flows. Fair values of trade receivables approximate their recorded

value.

Our financial instruments that are exposed to concentrations of credit risk consist primarily of

temporary cash investments, trade receivables, reinsurance recoverables and notes receivable. Limited

credit risk exists on trade receivables due to the diversity of our customer base and their dispersion

across broad geographic markets. We place our temporary cash investments with financial institutions

and limit the amount of credit exposure to any one financial institution.

We have mortgage receivables, which potentially expose us to credit risk. The portfolio of notes is

principally collateralized by self-storage facilities and commercial properties. We have not experienced

any material losses related to the notes from individual or groups of notes in any particular industry or

geographic area. The estimated fair values were determined using the discounted cash flow method and

using interest rates currently offered for similar loans to borrowers with similar credit ratings.

The carrying amount of long term debt and short term borrowings are estimated to approximate fair

value as the actual interest rate is consistent with the rate estimated to be currently available for debt of

similar term and remaining maturity.

Other investments including short term investments are substantially current or bear reasonable

interest rates. As a result, the carrying values of these financial instruments approximate fair value.

Assets and liabilities are recorded at fair value on the consolidated balance sheets and are measured

and classified based upon a three tiered approach to valuation. ASC 820 - Fair Value Measurements and

Disclosures (“ASC 820”) requires that financial assets and liabilities recorded at fair value be classified

and disclosed in one of the following three categories:

Level 1 – Unadjusted quoted prices in active markets that are accessible at the measurement date for

identical, unrestricted assets or liabilities;

Level 2 – Quoted prices for identical or similar financial instruments in markets that are not considered

to be active, or similar financial instruments for which all significant inputs are observable, either directly

or indirectly, or inputs other than quoted prices that are observable, or inputs that are derived principally

from or corroborated by observable market data through correlation or other means; and

Level 3 – Prices or valuations that require inputs that are both significant to the fair value

measurement and are unobservable. These reflect management’s assumptions about the assumptions a

market participant would use in pricing the asset or liability.