Time Warner Cable 2008 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2008 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

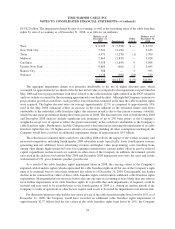

would have recorded an additional cable franchise rights impairment of approximately $4.74 billion; and had the

fair values of the cable franchise rights been lower by 30%, the Company would have recorded an additional cable

franchise rights impairment of approximately $7.11 billion. A decline in the fair values of the reporting units by up

to 30% would not result in any goodwill impairments, as the accounting rules first require a company to impair its

indefinite-lived intangible assets prior to testing for any goodwill impairments.

Long-lived Assets

Long-lived assets (e.g., customer relationships and property, plant and equipment) do not require that an

annual impairment test be performed; instead, long-lived assets are tested for impairment upon the occurrence of a

triggering event. Triggering events include the more likely than not disposal of a portion of such assets or the

occurrence of an adverse change in the market involving the business employing the related assets. Once a

triggering event has occurred, the impairment test is based on whether the intent is to hold the asset for continued

use or to hold the asset for sale. If the intent is to hold the asset for continued use, the impairment test first requires a

comparison of estimated undiscounted future cash flows generated by the asset group against the carrying value of

the asset group. If the carrying value of the asset group exceeds the estimated undiscounted future cash flows, the

asset would be deemed to be impaired. Impairment would then be measured as the difference between the estimated

fair value of the asset and its carrying value. Fair value is generally determined by discounting the future cash flows

associated with that asset. If the intent is to hold the asset for sale and certain other criteria are met (e.g., the asset can

be disposed of currently, appropriate levels of authority have approved the sale, and there is an active program to

locate a buyer), the impairment test involves comparing the asset’s carrying value to its estimated fair value. To the

extent the carrying value is greater than the asset’s estimated fair value, an impairment loss is recognized for the

difference.

Significant judgments in this area involve determining whether a triggering event has occurred, determining

the future cash flows for the assets involved and selecting the appropriate discount rate to be applied in determining

estimated fair value. In 2008, there were no significant long-lived asset impairments. However, as a result of the

impairment of cable franchise rights recorded during 2008, the Company determined a triggering event had

occurred and tested certain customer relationships for impairment in accordance with FASB Statement No. 144,

Accounting for the Impairment or Disposal of Long-Lived Assets, concluding that these customer relationships were

not impaired.

Investments

TWC’s investments are primarily accounted for using the equity method of accounting. A subjective aspect of

accounting for investments involves determining whether an other-than-temporary decline in value of the invest-

ment has been sustained. If it has been determined that an investment has sustained an other-than-temporary decline

in its value, the investment is written down to its fair value by a charge to earnings. This evaluation is dependent on

the specific facts and circumstances. TWC evaluates available information (e.g., budgets, business plans, financial

statements, etc.) in addition to quoted market prices, if any, in determining whether an other-than-temporary decline

in value exists. Factors indicative of an other-than-temporary decline include recurring operating losses, credit

defaults and subsequent rounds of financing at an amount below the cost basis of the Company’s investment. This

list is not all-inclusive and the Company weighs all known quantitative and qualitative factors in determining if an

other-than-temporary decline in the value of an investment has occurred. As discussed further in Note 10, during the

fourth quarter of 2008, the Company recorded a noncash pretax impairment of $367 million on its investment in

Clearwire LLC as a result of a significant decline in the estimated fair value of Clearwire, reflecting the Clearwire

Corp stock price decline from May 2008, when TWC agreed to make its investment.

Accounting for Pension Plans

TWC has both funded and unfunded noncontributory defined benefit pension plans covering a majority of its

employees. Pension benefits are based on formulas that reflect the employees’ years of service and compensation

99

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)