Time Warner Cable 2006 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2006 Time Warner Cable annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

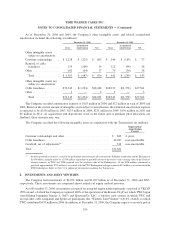

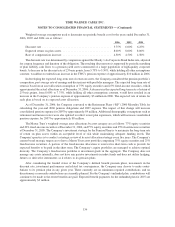

Weighted-average assumptions used to determine net periodic benefit cost for the years ended December 31,

2006, 2005 and 2004 are as follows:

2006 2005 2004

Discount rate ............................................ 5.75% 6.00% 6.25%

Expected return on plan assets. . .............................. 8.00% 8.00% 8.00%

Rate of compensation increase . .............................. 4.50% 4.50% 4.50%

The discount rate was determined by comparison against the Moody’s Aa Corporate Bond Index rate, adjusted

for coupon frequency and duration of the obligation. The resulting discount rate is supported by periodic matching

of plan liability cash flows to a pension yield curve constructed of a large population of high-quality corporate

bonds. A decrease in the discount rate of 25 basis points, from 5.75% to 5.50%, while holding all other assumptions

constant, would have resulted in an increase in the TWC’s pension expense of approximately $10 million in 2006.

In developing the expected long-term rate of return on assets, the Company considered the pension portfolio’s

composition, past average rate of earnings and discussions with portfolio managers. The expected long-term rate of

return is based on an asset allocation assumption of 75% equity securities and 25% fixed-income securities, which

approximated the actual allocation as of December 31, 2006. A decrease in the expected long-term rate of return of

25 basis points, from 8.00% to 7.75%, while holding all other assumptions constant, would have resulted in an

increase in the Company’s pension expense of approximately $3 million in 2006. The expected rate of return for

each plan is based on its expected asset allocation.

As of December 31, 2006, the Company converted to the Retirement Plans (“RP”) 2000 Mortality Table for

calculating the year-end 2006 pension obligations and 2007 expense. The impact of this change will increase

consolidated pension expense for 2007 by approximately $9 million. Additional demographic assumptions such as

retirement and turnover rates were also updated to reflect recent plan experience, which will increase consolidated

pension expense for 2007 by approximately $8 million.

The Master Trust’s weighted-average asset allocations by asset category are as follows: 77% equity securities

and 23% fixed-income securities at December 31, 2006, and 75% equity securities and 25% fixed-income securities

at December 31, 2005. The Company’s investment strategy for the Pension Plans is to maximize the long-term rate

of return on plan assets within an acceptable level of risk while maintaining adequate funding levels. The

Company’s practice is to conduct a strategic review of its asset allocation strategy every five years. The Company’s

current broad strategic targets are to have a Master Trust asset portfolio comprising 75% equity securities and 25%

fixed-income securities. A portion of the fixed-income allocation is reserved in short-term cash to provide for

expected benefits to be paid in the short term. The Company’s equity portfolios are managed to achieve optimal

diversity. The Company’s fixed-income portfolio is investment-grade in the aggregate. The Company does not

manage any assets internally, does not have any passive investments in index funds and does not utilize hedging,

futures or derivative instruments as it relates to its pension plans.

After considering the funded status of the Company’s defined benefit pension plans, movements in the

discount rate, investment performance and related tax consequences, the Company may choose to make contri-

butions to its pension plan in any given year. There currently are no minimum required contributions, and no

discretionary or noncash contributions are currently planned. For the Company’s unfunded plan, contributions will

continue to be made to the extent benefits are paid. Expected benefit payments for the unfunded plan for 2007 are

approximately $2 million.

136

TIME WARNER CABLE INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)