Starwood 2009 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2009 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

|

|

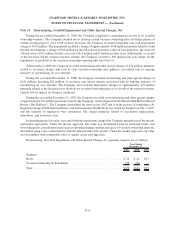

considered impaired. For the Company’s hotel reporting unit the fair value exceeded its carrying value. However,

the fair value of the vacation ownership reporting unit was less than its carrying value, as such goodwill was deemed

to be impaired, and step two of goodwill impairment test was performed. In the second step of the impairment test

the Company determined the implied fair value of goodwill for the vacation ownership reporting unit by deducting

the fair value of all tangible and intangible net assets as if it was acquired in a business combination, from the fair

value determined in step one. This step resulted in an implied goodwill fair value of $151 million compared to an

actual goodwill balance of $241 million, with the difference of $90 million representing the impairment charge. In

determining fair values associated with the goodwill impairment steps, the Company primarily used the income and

the market approaches. Under the income approach, fair value was determined based on the estimated future cash

flows of the reporting units taking into account assumptions such as, REVPAR, operating margins and sales pace of

vacation ownership units and discounting these cash flows using a discount rate commensurate with the risk

inherent in the calculations. Under the market approach, the fair value of the reporting units were determined based

on market valuation techniques such as comparable revenue and EBITDA multiples of similar companies in the

hospitality industry. The vacation ownership goodwill had not been previously impaired.

Based on the economic climate and the deterioration of results in the timeshare industry, it is reasonably

possible that the fair value of the vacation ownership segment could continue to decline, which could result in a

further impairment of its goodwill in the near term.

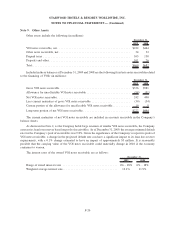

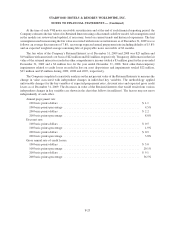

Intangible assets consisted of the following (in millions):

2009 2008

December 31,

Trademarks and trade names ......................................... $309 $315

Management and franchise agreements .................................. 376 354

Other . . . ....................................................... 76 90

761 759

Accumulated amortization ........................................... (181) (163)

$ 580 $ 596

The intangible assets related to management and franchise agreements have finite lives, and accordingly, the

Company recorded amortization expense of $35 million, $32 million and $26 million, respectively, during the years

ended December 31, 2009, 2008 and 2007. The other intangible assets noted above have indefinite lives.

Amortization expense relating to intangible assets with finite lives for each of the years ended December 31 is

expected to be as follows (in millions):

2010 . .................................................................. $36

2011 . .................................................................. $33

2012 . .................................................................. $32

2013 . .................................................................. $32

2014 . .................................................................. $32

F-19

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

NOTES TO FINANCIAL STATEMENTS — (Continued)