Samsung 2014 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2014 Samsung annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

059058

2014 Samsung Electronics Annual Report2014 Samsung Electronics Annual Report

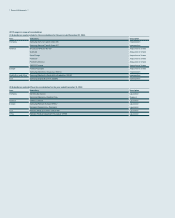

2.13 Impairment of Non-Financial Assets

Goodwill or intangible assets with indefinite useful lives are not subject to amorti-

zation and are tested annually for impairment. Assets that are subject to amortiza-

tion are reviewed for impairment whenever events or changes in circumstances

indicate that the carrying amount may not be recoverable. An impairment loss

is recognized for the amount by which the asset’s carrying amount exceeds its

recoverable amount. The recoverable amount is the higher of an asset’s fair value

less costs to sell and value in use. For the purposes of assessing impairment,

assets are grouped at the lowest levels for which there are separately identifiable

cash flows (cash-generating units). Non-financial assets other than goodwill for

which an impairment charge was previously recorded are reviewed for possible

reversal of the impairment at each reporting date.

2.14 Financial Liabilities

(A) Classification and measurement

Financial liabilities at fair value through profit or loss are financial instruments held

for trading. Financial liabilities are classified in this category if incurred principally

for the purpose of repurchasing them in the near term. Derivatives that are not

designated as hedges or bifurcated from financial instruments containing embed-

ded derivatives are also categorized as held-for-trading.

The Group classifies non-derivative financial liabilities, except for financial liabili-

ties at fair value through profit or loss, financial guarantee contracts and financial

liabilities that arise when a transfer of financial assets does not qualify for derecog-

nition, as financial liabilities carried at amortized cost and presented as ‘trade

payables’, ‘borrowings’, and ‘other financial liabilities’ in the statement of financial

position.

(B) Derecognition

Financial liabilities are removed from the statement of financial position when they

are extinguished, for example, when the obligation specified in the contract is dis-

charged, cancelled or expires or when the terms of an existing financial liability are

substantially modified.

2.15 Trade Payables

Trade payables are amounts due to suppliers for merchandise purchased or ser-

vices received in the ordinary course of business. If payment is expected in one

year or less, they are classified as current liabilities. If payment is expected beyond

one year, they are presented as non-current liabilities. Non-current trade payables

are recognized initially at fair value and subsequently measured at amortized cost

using the effective interest method.

2.16 Borrowings

Borrowings are recognized initially at fair value, net of transaction costs, and are

subsequently measured at amortized cost. Any difference between cost and the

redemption value is recognized in the statement of income over the period of the

borrowings using the effective interest method. If the Group has an indefinite right

to defer payment for a period longer than 12 months after the end of the reporting

date, such liabilities are recorded as non-current liabilities, otherwise, they are re-

corded as current liabilities.

2.17 Provisions

A provision is recognized when the Group has a present legal or constructive

obligation as a result of a past event, it is probable that an outflow of resources

embodying economic benefits will be required to settle the obligation, and a re-

liable estimate can be made of the amount of the obligation. Provisions are not

recognized for future operating losses.

Provisions are measured at the present value of the expenditures expected to be

required to settle the obligation using a pre-tax rate that reflects current market as-

sessments of the time value of money and the risks specific to the obligation. The

increase in the provision due to passage of time is recognized as interest expense.

When it is probable that an outflow of economic benefits will occur due to a pres-

ent obligation resulting from a past event, and the amount is reasonably estimable,

a corresponding provision is recognized in the financial statements. However,

when such outflow is dependent upon a future event that is not certain to occur,

or cannot be reliably estimated, a disclosure regarding the contingent liability is

made in the notes to the financial statements.

2.18 Net Defined Benefit Liabilities

The Group has a variety of retirement pension plans including defined benefit and

defined contribution plans. A defined contribution plan is a pension plan under

which the Group pays fixed contributions into a separate entity. The Group has

no legal or constructive obligations to pay further contributions if the fund does

not hold sufficient assets to pay all employees the benefits relating to employee

service in the current and prior periods. For defined contribution plans, the Group

pays contributions to annuity plans that are managed either publicly or privately

on a mandatory, contractual or voluntary basis. The Group has no further future

payment obligations once the contributions have been paid. The contributions are

recognized as employee benefit expense when they are due. Prepaid contribu-

tions are recognized as an asset to the extent that a cash refund or a reduction in

the future payments is available.

A defined benefit plan is a pension plan that is not a defined contribution plan. Typ-

ically defined benefit plans define an amount of pension benefit that an employee

will receive on retirement, usually dependent on one or more factors such as age,

years of service and compensation. The liability recognized in the statement of

financial position in respect to defined benefit pension plans is the present value of

the defined benefit obligation at the end of the reporting period less the fair value

of plan assets. The defined benefit obligation is calculated annually by indepen-

dent actuaries using the projected unit credit method. The present value of the

defined benefit obligation is determined by discounting the estimated future cash

outflows using interest rates of high-quality corporate bonds that are denominated

in the currency in which the benefits will be paid and that have terms to maturity

approximating to the terms of the related pension obligation.

Actuarial gains and losses resulting from the changes in actuarial assumptions, and

the differences between the previous actuarial assumptions and what has actually

occurred, are recognized in other comprehensive income in the period in which

they were incurred. Past service costs are immediately recognized in profit or loss.