PG&E 2007 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2007 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

94

to design, estimate, and schedule work. PG&E Corporation

and the Utility amortize capitalized software costs ratably

over the expected lives of the software ranging from 3 to

15 years, commencing upon operational use.

REGULATION AND STATEMENT OF

FINANCIAL ACCOUNTING STANDARDS NO. 71

PG&E Corporation and the Utility account for the fi nancial

effects of regulation in accordance with SFAS No. 71. SFAS

No. 71 applies to regulated entities whose rates are designed

to recover the costs of providing service. SFAS No. 71 applies

to all of the Utility’s operations.

Under SFAS No. 71, incurred costs that would otherwise

be charged to expense may be capitalized and recorded as

regulatory assets if it is probable that the incurred costs will

be recovered in rates in the future. The regulatory assets are

amortized over future periods consistent with the inclusion

of costs in authorized customer rates. If costs that a regu-

lated enterprise expects to incur in the future are currently

being recovered through rates, SFAS No. 71 requires that

the regulated enterprise record those expected future costs as

regulatory liabilities. In addition, amounts that are probable

of being credited or refunded to customers in the future

must be recorded as regulatory liabilities.

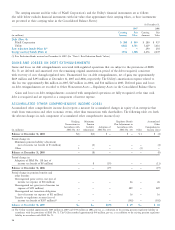

INTANGIBLE ASSETS

Intangible assets consist of hydroelectric facility licenses

and other agreements, with lives ranging from 19 to

40 years. The gross carrying amount of the hydroelectric

facility licenses and other agreements was approximately

$97 million at December 31, 2007 and $73 million at

December 31, 2006. The accumulated amortization was

approximately $32 million at December 31, 2007 and

$28 million at December 31, 2006.

The Utility’s amortization expense related to intangible

assets was approximately $3 million in 2007, 2006, and 2005.

The estimated annual amortization expense based on the

December 31, 2007 intangible asset balance for the Utility’s

intangible assets for 2008 through 2012 is approximately

$3 million each year. Intangible assets are recorded to Other

Noncurrent Assets in the Consolidated Balance Sheets.

CONSOLIDATION OF

VARIABLE INTEREST ENTITIES

The Financial Accounting Standards Board (“FASB”)

Interpretation No. 46 (revised December 2003), “Consolida-

tion of Variable Interest Entities” (“FIN 46R”), provides that

an entity is a variable interest entity (“VIE”) if it does not

have suffi cient equity investment at risk, or if the holders of

the entity’s equity instruments lack the essential characteris-

tics of a controlling fi nancial interest. FIN 46R requires that

the holder subject to the majority of the risk of loss from

a VIE’s activities must consolidate the VIE. However, if no

holder has the majority of the risk of loss, then a holder

entitled to receive a majority of the entity’s residual returns

would consolidate the entity.

The nature of power purchase agreements is such that

the Utility could have a signifi cant variable interest in a

power purchase agreement counterparty if that entity is a

VIE owning one or more plants that sell substantially all of

their output to the Utility, and the contract price for power

is correlated with the plant’s variable costs of production.

In 2007, the Utility entered into a 25-year agreement to

purchase as-available electric generation output from a new

approximately 554-megawatt (“MW”) solar trough facility

in which the Utility has a signifi cant variable interest.

Activities of this facility consist of renewable energy

production from a single facility for sale to third parties.

The Utility is not considered the primary benefi ciary for

this VIE, as it will not absorb the majority of the entity’s

expected losses or residual returns. Accordingly, the Utility

will not consolidate this VIE in its consolidated fi nancial

statements. This project is expected to become operational

in 2011 and no payments for energy have been made to

this facility as of December 31, 2007. Future payments

to this facility are expected to be recoverable through

customer rates.

IMPAIRMENT OF LONG-LIVED ASSETS

The carrying values of long-lived assets are evaluated

in accordance with the provisions of SFAS No. 144,

“Accounting for the Impairment of Long Lived Assets”

(“SFAS No. 144”). In accordance with SFAS No. 144, PG&E

Corporation and the Utility evaluate the carrying amounts

of long-lived assets for impairment whenever events occur

or circumstances change that may affect the recoverability or

the estimated life of long-lived assets. No signifi cant impair-

ments were recorded in 2007, 2006, and 2005.

ASSET RETIREMENT OBLIGATIONS

PG&E Corporation and the Utility account for ARO in

accordance with SFAS No. 143, “Accounting for Asset

Retirement Obligations” (“SFAS No. 143”) and FASB

Interpretation No. 47, “Accounting for Conditional Asset

Retirement Obligations — an Interpretation of FASB State-

ment No. 143” (“FIN 47”). SFAS No. 143 requires that an

asset retirement obligation be recorded at fair value in the

period in which it is incurred if a reasonable estimate of