PG&E 2007 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2007 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

48

PG&E Corporation and the Utility seek to maintain or

strengthen their credit ratings in order to provide liquidity

through effi cient access to fi nancial and trade credit, and to

reduce fi nancing costs. PG&E Corporation and the Utility

also seek to maintain the Utility’s CPUC-authorized capital

structure, which includes a 52% common equity component.

In 2007, Moody’s upgraded the Utility’s credit rating to A3,

thereby terminating a provision in the Chapter 11 Settlement

Agreement that had required the CPUC to authorize a mini-

mum 52% common equity ratio and a minimum ROE for

the Utility of 11.22% until the Utility received a credit rat-

ing of A3 from Moody’s or A- from S&P. On December 20,

2007, the CPUC issued a decision maintaining the Utility’s

authorized ROE at 11.35% and its common equity compo-

nent at 52% for 2008.

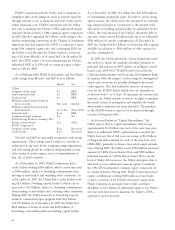

As of February 2008, PG&E Corporation’s and the Utility’s

credit ratings from Moody’s and S&P were as follows:

Moody’s S&P

Utility

Corporate credit rating A3 BBB+

Senior unsecured debt A3 BBB+

Credit facility A3 BBB+

Pollution control bonds backed by

letters of credit Not rated AA/A-1+

Pollution control bonds backed by

bond insurance A3 to Aaa AA to AAA

Preferred stock Baa2 BBB-

Commercial paper program P-2 A-2

PG&E Energy Recovery Funding LLC

Energy recovery bonds Aaa AAA

PG&E Corporation

Corporate credit rating Baa1 Not rated

Credit facility Baa1 Not rated

Moody’s and S&P are nationally recognized credit rating

organizations. These ratings may be subject to revision or

withdrawal at any time by the assigning rating organization

and each rating should be evaluated independently of any

other rating. A credit rating is not a recommendation to

buy, sell, or hold securities.

As of December 31, 2007, PG&E Corporation had a

credit facility totaling $200 million, which can be increased

to $300 million, subject to obtaining commitments from

existing or new lenders and satisfying other conditions. As

of December 31, 2007, the Utility had a credit facility total-

ing $2.0 billion (“working capital facility”), which can be

increased to $3.0 billion, subject to obtaining commitments

from existing or new lenders and satisfying other conditions.

During 2007, the Utility increased its borrowing capacity

under its commercial paper program from $1.0 billion

to $1.75 billion. As of December 31, 2007, the Utility had

$165 million of letters of credit and $250 million of

borrowings outstanding under its working capital facility.

As of December 31, 2007, the Utility also had $270 million

of outstanding commercial paper. In order to satisfy rating

agency criteria, the Utility treats the amount of its outstand-

ing commercial paper as a reduction to the amount avail-

able under its working capital facility. As authorized by the

CPUC, the total amount of the Utility’s short-term debt at

any time cannot exceed $2 billion (plus up to an additional

$500 million for specifi c contingencies). At December 31,

2007, the Utility had $1.3 billion of short-term debt capacity

available (in addition to $500 million of debt capacity for

specifi c contingencies).

In 2005, the Utility purchased a fi nancial guaranty insur-

ance policy to insure the regularly scheduled payment of

principal and interest on $454 million of pollution control

bonds series 2005 A-G (“PC2005 bonds”) issued by the

California Infrastructure and Economic Development Bank.

In January 2008, the insurer’s credit rating was downgraded

and/or put on review for possible downgrade by several

credit agencies. This has resulted in increases in interest

rates for the PC2005 bonds, which rates are currently set

at auction every 7 or 35 days. To minimize this interest rate

exposure, the Utility intends to exercise its right to purchase

the bonds in lieu of redemption and remarket the bonds

when market conditions are more favorable. The purchase

of the PC2005 bonds is expected to be fi nanced through

issuance of long-term debt.

As discussed below in “Capital Expenditures,” the

Utility expects that its capital expenditures will average

approximately $3.4 billion over each of the next four years.

Subject to additional CPUC authorization as needed, the

Utility forecasts that it will issue an average of $1.4 billion

of long-term debt annually for each of the next four years

(2008–2011), primarily to fi nance forecasted capital expendi-

tures. During 2007, the Utility issued $700 million principal

amount of 5.80% 30-year Senior Notes and $500 million

principal amount of 5.625% 10-year Senior Notes. As the

level of Utility debt increases, the Utility anticipates that it

will need to issue additional common equity to maintain

the 52% CPUC-authorized common equity component of

its capital structure. During 2007, PG&E Corporation made

equity contributions totaling $400 million to the Utility

to meet a portion of the Utility’s forecasted equity needs.

PG&E Corporation anticipates that it will contribute

$2 billion to $2.5 billion of additional equity to the Utility

over the next four years to maintain the Utility’s CPUC-

authorized capital structure.