GameStop 2013 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2013 GameStop annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

|

|

F-14

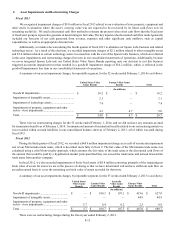

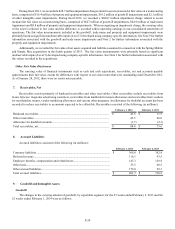

are accounted for on a straight-line basis over the lease term, which includes renewal option periods when we are reasonably

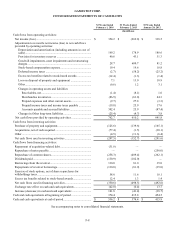

assured of exercising the renewal options and includes “rent holidays” (periods in which we are not obligated to pay rent). Cash

or lease incentives received upon entering into certain store leases (“tenant improvement allowances”) are recognized on a straight-

line basis as a reduction to rent expense over the lease term, which includes renewal option periods when we are reasonably assured

of exercising the renewal options. We record the unamortized portion of tenant improvement allowances as a part of deferred rent.

We do not have leases with capital improvement funding. Percentage rentals are based on sales performance in excess of specified

minimums at various stores and are accounted for in the period in which the amount of percentage rentals can be accurately

estimated.

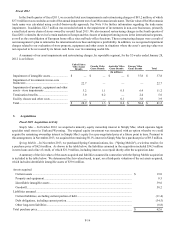

Foreign Currency Translation

We have determined that the functional currencies of our foreign subsidiaries are the subsidiaries’ local currencies. The

assets and liabilities of the subsidiaries are translated at the applicable exchange rate as of the end of the balance sheet date and

revenue and expenses are translated at an average rate over the period. Currency translation adjustments are recorded as a component

of other comprehensive income. Transaction and derivative net gains (losses) are included in selling, general and administrative

expenses and were $3.3 million, $2.5 million and $(0.6) million for the 52 weeks ended February 1, 2014, the 53 weeks ended

February 2, 2013 and the 52 weeks ended January 28, 2012, respectively. The foreign currency transaction gains and losses are

primarily due to the decrease or increase in the value of the U.S. dollar compared to the functional currencies of the countries in

which we operate internationally. The foreign currency transaction gains and (losses) are primarily due to fluctuations in the value

of the U.S. dollar compared to the Australian dollar, Canadian dollar and euro.

We use forward exchange contracts, foreign currency options and cross-currency swaps (together, the “foreign currency

contracts”) to manage currency risk primarily related to intercompany loans denominated in non-functional currencies and certain

foreign currency assets and liabilities. These foreign currency contracts are not designated as hedges and, therefore, changes in

the fair values of these derivatives are recognized in earnings, thereby offsetting the current earnings effect of the re-measurement

of related intercompany loans and foreign currency assets and liabilities (see Note 6).

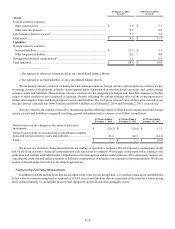

New Accounting Pronouncements

In July 2013, the Financial Accounting Standards Board ("FASB") issued an Accounting Standards Update (“ASU”) related

to the presentation of unrecognized tax benefits when a net operating loss carryforward, a similar tax loss, or a tax credit carryforward

exists. The ASU requires an unrecognized tax benefit, or a portion of an unrecognized tax benefit, to be presented in the financial

statements as either a reduction to a deferred tax asset or separately as a liability depending on the existence, availability and/or

use of an operating loss carryforward, a similar tax loss, or a tax credit carryforward. This ASU will be effective for us beginning

the first quarter of 2014. We do not expect that this ASU will have an impact on our consolidated financial statements as we

currently do not have any unrecognized tax benefits in the same jurisdictions in which we have tax loss or credit carryovers.

In March 2013, the FASB issued an ASU providing guidance with respect to the release of cumulative translation adjustments

into net income when a parent company sells either a part or all of an investment in a foreign entity. The ASU requires the release

of cumulative translation adjustments when a company no longer holds a controlling financial interest in a foreign subsidiary or

a group of assets that constitutes a business within a foreign entity. This ASU will be effective for us beginning the first quarter

of 2014. We are evaluating the effect of this ASU, but do not expect it to have a significant impact on our Consolidated Financial

Statements.

In February 2013, the FASB issued an ASU related to the reporting and disclosure of amounts reclassified out of accumulated

other comprehensive income by component. An entity is required to present either on the face of the statement of operations or

in the notes, significant amounts reclassified out of accumulated other comprehensive income by the respective line items of net

income, but only if the amount reclassified is required to be reclassified to net income in its entirety in the same reporting period.

For amounts not reclassified in their entirety to net income, an entity is required to cross-reference to other disclosures that provide

additional detail about those amounts. This ASU was effective for our annual and interim periods beginning in fiscal 2013. The

ASU had no effect on our consolidated financial statements as we have a single component of other comprehensive income,

currency translation adjustments, which is not reclassified to net income.