Berkshire Hathaway 2012 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2012 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

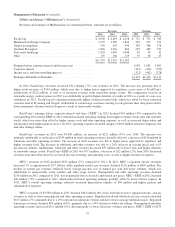

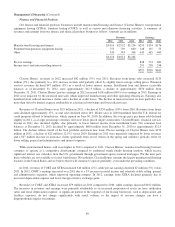

Management’s Discussion (Continued)

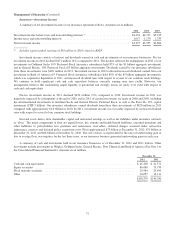

Finance and Financial Products

Our finance and financial products businesses include manufactured housing and finance (Clayton Homes), transportation

equipment leasing (XTRA), furniture leasing (CORT) as well as various miscellaneous financing activities. A summary of

revenues and earnings from our finance and financial products businesses follows. Amounts are in millions.

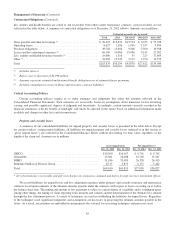

Revenues Earnings

2012 2011 2010 2012 2011 2010

Manufactured housing and finance .................................. $3,014 $2,932 $3,256 $255 $154 $176

Furniture/transportation equipment leasing ............................ 753 739 660 148 155 53

Other .......................................................... 343 343 348 445 465 460

$4,110 $4,014 $4,264

Pre-tax earnings ................................................. 848 774 689

Income taxes and noncontrolling interests ............................. 291 258 248

$557 $516 $441

Clayton Homes’ revenues in 2012 increased $82 million (3%) over 2011. Revenues from home sales increased $129

million (9%), due primarily to a 14% increase in units sold partially offset by slightly lower average selling prices. Financial

services revenues declined $47 million (3%) as a result of lower interest income. Installment loan and finance receivable

balances as of December 31, 2012, were approximately $12.3 billion, a decline of approximately $550 million from

December 31, 2011. Clayton Homes’ pre-tax earnings in 2012 increased $101 million (66%) over earnings in 2011. Earnings in

2012 were impacted by the increased unit sales which improved manufacturing and other operating efficiencies. Earnings also

benefited from reduced insurance claims and a decline in credit losses. The decline in interest income on loan portfolios was

more than offset by interest expense attributable to a decline in borrowings and lower interest rates.

Revenues of Clayton Homes were $2.9 billion in 2011, a decline of $324 million (10%) from 2010. Revenues from home

sales declined approximately 17%, as unit sales declined about 14%. Home sales in 2010 benefitted from the U.S. federal tax

credit program offered to homebuyers, which expired on June 30, 2010. In addition, the average price per home sold declined

slightly in 2011, as a larger percentage of homes sold were lower priced single section units. Clayton Homes’ financial services

income in 2011 also declined slightly, due primarily to lower interest income from installment loans. Net consumer loan

balances at December 31, 2011 declined by approximately $600 million from December 31, 2010 to approximately $12.9

billion. The decline reflects runoff of the loan portfolio and fewer new loans. Pre-tax earnings of Clayton Homes were $154

million in 2011, a decline of $22 million (12.5%) versus 2010. Earnings in 2011 were negatively impacted by lower revenues

and a $27 million increase in insurance claims (primarily from severe storms in the spring and summer), partially offset by

lower selling, general and administrative and interest expenses.

While manufactured homes sold were higher in 2012 compared to 2011, Clayton Homes’ manufactured housing business

continues to operate at a competitive disadvantage compared to traditional single family housing markets, which receive

significant interest rate subsidies from the U.S. government through government agency insured mortgages. For the most part,

these subsidies are not available to factory built homes. Nevertheless, Clayton Homes remains the largest manufactured housing

business in the United States and we believe that it will continue to operate profitably, even under the prevailing conditions.

In 2012, revenues of CORT and XTRA increased $14 million (2%), while pre-tax earnings declined $7 million (5%) versus

2011. In 2012, CORT’s earnings increased over 2011 due to a 5% increase in rental income and relatively stable selling, general

and administrative expenses, which improved operating margins. In 2012, earnings from XTRA declined primarily due to

increased depreciation expense and lower foreign currency exchange gains.

Revenues of CORT and XTRA increased $79 million in 2011 compared to 2010, while earnings increased $102 million.

The increases in revenues and earnings were primarily attributable to an increased proportion of assets on lease (utilization

rates) and lower depreciation expense. A significant portion of the expenses of our leasing businesses, such as depreciation and

facilities expenses, do not change significantly with rental volume, so the impact of revenue changes can have a

disproportionate impact on earnings.

80