Berkshire Hathaway 2012 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2012 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

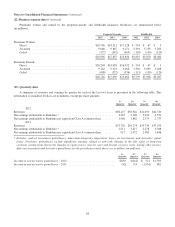

Management’s Discussion (Continued)

Insurance—Underwriting (Continued)

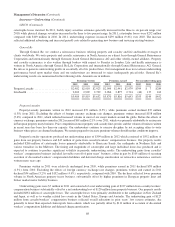

GEICO

Through GEICO, we primarily write private passenger automobile insurance, offering coverages to insureds in all 50 states

and the District of Columbia. GEICO’s policies are marketed mainly by direct response methods in which customers apply for

coverage directly to the company via the Internet or over the telephone. This is a significant element in our strategy to be a low-

cost auto insurer. In addition, we strive to provide excellent service to customers, with the goal of establishing long-term

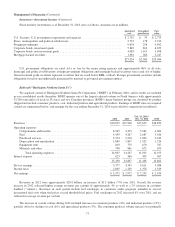

customer relationships. GEICO’s underwriting results are summarized below. Dollars are in millions.

2012 2011 2010

Amount % Amount % Amount %

Premiums written ........................................... $17,129 $15,664 $14,494

Premiums earned ............................................ $16,740 100.0 $15,363 100.0 $14,283 100.0

Losses and loss adjustment expenses ............................ 12,700 75.9 12,013 78.2 10,631 74.4

Underwriting expenses ....................................... 3,360 20.0 2,774 18.1 2,535 17.8

Total losses and expenses ..................................... 16,060 95.9 14,787 96.3 13,166 92.2

Pre-tax underwriting gain ..................................... $ 680 $ 576 $ 1,117

Premiums earned in 2012 were approximately $16.7 billion, an increase of $1,377 million (9.0%) over 2011. The growth in

premiums earned for voluntary auto was 9.0% as a result of a 6.5% increase in policies-in-force and an increase in average

premium per policy over the past twelve months. Voluntary auto new business sales in 2012 increased slightly compared with

2011. Voluntary auto policies-in-force at December 31, 2012 were approximately 704,000 greater than at December 31, 2011.

Losses and loss adjustment expenses incurred in 2012 were $12.7 billion, an increase of $687 million (5.7%) over 2011.

Our loss ratio (the ratio of losses and loss adjustment expenses incurred to premiums earned) was 75.9% in 2012 and 78.2% in

2011. We incurred losses (net of estimated salvage) of $490 million from Hurricane Sandy in the fourth quarter of 2012. For the

year, catastrophe losses were $638 million (3.8 loss ratio points) in 2012 compared to $252 million (1.6 loss ratio points) in

2011. Our loss ratio declined in 2012 as compared to 2011. Claims frequencies for property damage and collision coverages

were down about one percent, comprehensive coverage frequencies were down about ten percent, excluding Hurricane Sandy,

and frequencies for bodily injury coverages were relatively unchanged. In 2012, frequencies were lower in the second half of the

year than they were in the first half. Physical damage severities increased in the two to four percent range and bodily injury

severities increased in the one to three percent range from 2011.

Underwriting expenses incurred in 2012 increased $586 million (21.1%) compared with 2011. The increase was primarily

the result of a change in U.S. GAAP concerning deferred policy acquisition costs (“DPAC”). DPAC represents the underwriting

costs that are eligible to be capitalized and expensed as premiums are earned over the policy period. Upon adoption of the new

accounting standard as of January 1, 2012, GEICO ceased deferring a large portion of its advertising costs. The new accounting

standard was adopted on a prospective basis and as a result, DPAC recorded as of December 31, 2011 was amortized to expense

over the remainder of the related policy periods in 2012. Policy acquisition costs related to policies written and renewed after

December 31, 2011 are being deferred at lower levels than in the past. The new accounting standard for DPAC does not impact

the cash basis periodic underwriting costs or our assessment of GEICO’s underwriting performance. However, the new

accounting standard accelerates the timing of when certain underwriting costs are recognized in earnings. We estimate that

GEICO’s underwriting expenses in 2012 would have been about $410 million less had we computed DPAC under the prior

accounting standard and that, as a result, GEICO’s expense ratio (the ratio of underwriting expenses to premiums earned) in

2012 would have been less than in 2011.

Premiums earned in 2011 increased $1,080 million (7.6%) over 2010. Voluntary auto policies-in-force increased

approximately 7.0% as compared to 2010. The increase in policies-in-force in 2011 reflected an increase of 9.4% in voluntary

auto new business sales. Voluntary auto policies-in-force at December 31, 2011 were approximately 709,000 greater than at

December 31, 2010.

Losses and loss adjustment expenses incurred in 2011 increased $1,382 million (13.0%) as compared to 2010, increasing at

a greater rate than premiums earned. As a result, the loss ratio increased from 74.4% in 2010 to 78.2% in 2011. The increase in

the loss ratio in 2011 was primarily due to higher average injury and physical damage severities estimates and increased

67